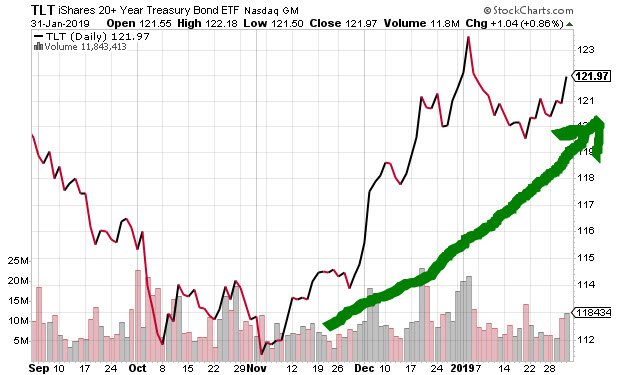

1987?

Don't be superstitious, it's not a repeat of 1987, but it could be a mini version!

Good earnings provide more fuel for this great January rally the best in 32 years.

Trade negotiations progress - even minor - as well as spin, can take market to the SPX 200ma tomorrow

If shutdown negotiations in Congress can be concluded successfully and there continues to be good earnings report then SPX 2800 can be reached in February.

But, I am looking for a pullback during the next 2 to 3 trading days. What happens after that will be very important: will it resume this strong rally or will it reverse down 5 to 10%

I am building a big QQQ JUNE Put position, at least 40 puts by the times SPX reaches SPX 2740. I expect SPX 2500 or lower by late February or early March.

Don't be fooled by a record January for the markets https://bloom.bg/2UwUp4K via @bopinion

Market historians are likely to remember January 2019 for years to come. Not only did the S&P 500 Index turn in its best start to a year since 1987 by surging 7.87 percent, but global equities, bonds and commodities all generated positive returns in the same month for the first time since last January. But that’s where the similarities between the moves end, which is too bad.

The MSCI All-Country World Index of equities has jumped 7.80 percent, while the Bloomberg Barclays Global Aggregate Bond Index was up 0.92 percent through Wednesday and the Bloomberg Commodity Index has surged 5.23 percent. Those just returning from an Elon Musk-sponsored flight to Mars might look at the financial markets and conclude that all is right in the world. In reality, the gains are coming when global economic growth is rapidly decelerating to the point where central bankers are being forced to delay their plans to normalize monetary policies. That’s far different from this time last year, when the buzzwords were global synchronized economic recovery and tighter monetary policy. But as we know, 2018 turned out to be a terrible year for stocks, bonds and commodities, showing that good beginnings don’t always end well. (Everyone remembers what happened in 1987, right?) Will 2019 turn out different? Anything’s possible, but the odds are long given that the recent gains have more to do with relief that the Federal Reserve has had a change of heart and is less likely to cause a recession through excessive interest-rate hikes. But that still leaves a slowing economy no longer supported by either tax cuts or surging corporate profits, which doesn’t engender a lot of confidence