A Critical Analysis of Robert Prechter and Elliott Wave International

(March 2009-Present)

PART 2

In the first installment of this series, I examined Robert Prechter and Elliott Wave International's current wave analysis and proposed some alternate views. In this segment I will examine EWI's market timing record. First, I'll run down the history of EWI's market calls from March 2009 to present. In conclusion, I will analyze a few of the flaws in trading methodology which led to the failed trading results documented here. In subsequent installments of this review I'll analyze larger issues of data and epistemological methodology that underly EWI's conclusions of a deflationary depression.

The source material for this study is the Elliott Wave Theorist (EWT) and Elliott Wave Financial Forecast (EWFF) as well as numerous writings and audio and video interviews with Robert Prechter and Steve Hochberg. For the sake of simplicity this body of work will be referred to as "EWI". Bold emphasis in quoted text is mine to illustrate key points. All EWI images are drawn from freely available material published online and are linked to their sources.

To get the most out of this piece it's best to have a basic understanding of Elliott Wave theory. I selected this tutorial at random from among the many available on the web: http://www.tradingfi...eory-basics.htm.

II. Market Timing

SUMMARY

For reasons of time and space and access to insufficient data I'll have to limit the parameters of this discussion to the period of March 2009 to the present. It's clear that EWI did call a bottom in the US stock markets in late February of 2009 and recommended to subscribers that they cover short positions at that time. Since then Robert Prechter has recommended that subscribers enter 200% fully leveraged short positions on at least three occasions. There is no evidence that EWI has ever called for those short trading positions to be covered and they are assumed to be still open at a substantial net loss. Elliott Wave Financial Forecast has maintained a Primary and Intermediate degree short position going back to at least September 2010 but evidence suggests that that position goes back considerably further, perhaps all the way back to September 2009. Some of the problems of trading methodology leading to the failed results documented here are: a lack of trading discipline, particularly no use of stop losses; a consistent practice of "top picking"; a tendency to regard market analysis as an intellectual exercise rather than a profit making endeavour.

ANALYSIS

Bob Prechter and EWI have been calling the top of the presumed corrective wave from the March 2009 low since August of 2009. In July 2009 they began to anticipate the end of the now 23 month long rally after just 4 months:

On February 23, EWT called for the S&P to bottom in the 600s and then begin a sharp rally, the biggest since the 2007 high. The S&P bottomed at 667 on March 6. Then the stock market and commodities went almost straight up for three months as the dollar fell

.The June 11 issue called for interim tops in stocks, metals and oil and a temporary bottom in the dollar. The Dow topped that day and fell nearly 800 points; silver reversed and fell from $16 to $12.45; gold slid about $90; and oil, which had just doubled, reversed and fell from $73.38 to $58.32. The dollar simultaneously rallied and traced out a triangle for wave 4. Bonds bounced as well

.Corrective patterns can be complex, so we should hesitate to be too specific about the shape this bear market rally will take. But from lows on July 8 (intraday) and 10 (close), the stock market may have begun the second phase of advance that will fulfill our ideal scenario for a three-wave (up-down-up) rally. (07/09 EWT; The Bounce Is Aging, But The Depression Is Young)

Now in his August 2009 Theorist, Bob explains what "the prudent thing to do" in the markets is, based on the same Elliott wave pattern and sentiment indicators -- plus the Dow's 3/8 Fibonacci retracement from the March 9 low...Bob Prechter's August Elliott Wave Theorist published a week and a half early: he did so to give subscribers time to prepare for what's ahead. The issue provides a list of levels that mark Fibonacci and Elliott-wave related retracements for the rally. He analyzes which one is the most likely end point, and even explains how you can make the most of the waning rally. Prechter Stands Alone Again... He's Done the Math

The Dow has just entered the lower end of its upside target range we cited back in April; the S&P is close behind. Restored optimism for a lengthy recovery at worst a new bull market at best is one of several signs of an important peak. All the same markets that recovered together have now set the stage to decline together. And this time there will be no mistake about the next wave down. It will be a "third of a third," also known as the point of recognition. (08/09 EWFF; 'Worst Is Over' Optimism Sets Up Volatile Third Wave Surprise)

The stock market has been in an upward correction for over two months. Evidence is quite strong that the rally is over. (08/09 EWFF)

WATCH VIDEO: Bob Prechter on CNBC August 17, 2009 calling an end to the rally.

Here's what the market looked like at that time, with the EWI wave count.

So by mid-August of 2009, EWI called a Wave 2 top following a 38.2% Fibonacci retracement of the decline from the October 2007 high. The market immediately turned higher.

In September 2009, the warning flag of an imminent Wave 3 decline was still out in spite of yet higher highs:

How A Bear Can Be Bullish And Still Be Right

http://www.marketora...ticle13310.html The Zaniness of 1999 and 2000 is Back EWI's view of the market at that time: How A Bear Can Be Bullish And Still Be Right: "April 2009 Elliott Wave Financial Forecast calculated a specific target range for the Dow's rally: the 9,000-10,000 level."

How A Bear Can Be Bullish And Still Be Right: "April 2009 Elliott Wave Financial Forecast calculated a specific target range for the Dow's rally: the 9,000-10,000 level."In October 2009, EWI sensationally compared the market at that time to the Dow in 1929: Black Monday: Ancient History Or Imminent Future?. Once again, a top was called.

Yet the extremes in optimism as measured by unanimously bullish investor surveys and exuberant sentiment readings point to a dying rally. Momentum and breadth readings support that case, as do telling Elliott wave patterns. From a socionomic standpoint, investor mood has returned to levels of enthusiasm we saw at the high just as Elliott-minded investors would expect from a wave 2 rally. Once again, EWI analysts are virtually alone in their deflationary forecasts. This issue demonstrates why the mainstream conventional wisdom just as it did at the top in October 2007 and the bottom in March 2009 will again miss a major reversal on the horizon. (10/09 EWFF, What to Read When 'Everyone' is Bullish)

[The week of Oct. 12, 2009], the Dow touched 10,000 and the S&P hit 1095, reaching the upper end of our range for a normal rally and fulfilling our original expectations from last March-April. (10/09 EWT; How to Prepare Yourself for the 'Serious Event' Ahead)

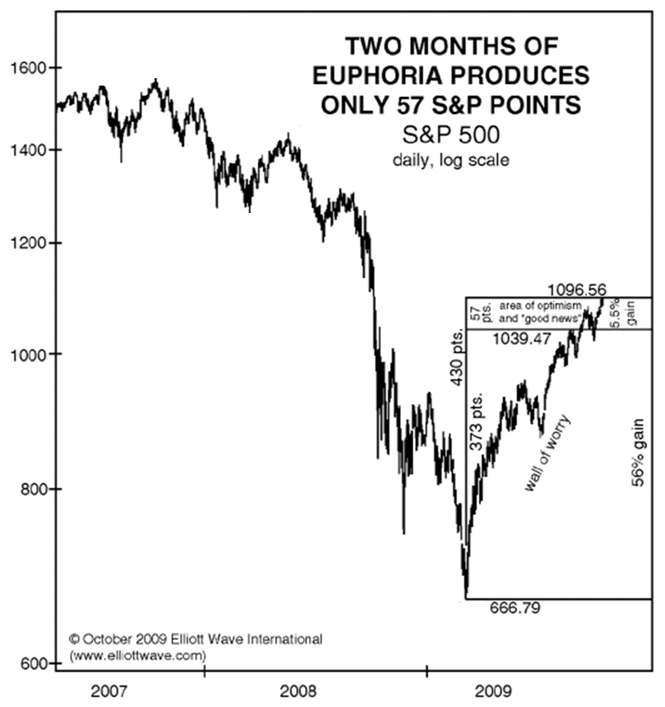

This chart from the October 2009 Elliott Wave Theorist attempts to illustrate a rally that is topping due to declining momentum:

This S&P 500 Chart Tells the Two-Part Truth:

You see when most of the rally unfolded. Six months of serious worry produces a 373-point climb, whereas "two months of euphoria produces only 57 S&P points." Now, the two-part truth about this rally is an easy story to tell. It's literally a few lines and notations on a price chart. Yet have you seen or read ANYTHING like this in the past two weeks? Has anyone else pointed out that over the past two months, the stock market "rally" has in fact slowed to a crawl?

Eight months ago, the stock market began a very large rally -- the gains exceeded 60% in the S&P 500. Everyone knows this. But here's a fact that has gone virtually unreported: The vast majority of those gains (about 90%) were from March through August. By comparison, September and October were sluggish.

Yet the past two months have been the very time when the financial press has been the loudest about "green shoots," "recovery" and "new bull market." So the question is WHY -- why so much enthusiasm, even as the evidence literally fades away?

No one asks questions like this, never mind provides the answers. The one exception is Bob Prechter. And if most investors suddenly DID learn the details of his answer... well, the information would buckle their knees.

Prechter does of course provide a detailed answer in his current Elliott Wave Theorist. The latest Elliott Wave Financial Forecast expands on that answer. You can read both award-winning monthly market letters right now for free!

But let me be clear: The answer is in fact a forecast. What Prechter says is bigger and more important than these two publications. It could prove to be the most important forecast he has offered since the financial debacle began. (Robert Prechter Latest Financial Market Analysis)

We do know one thing: When everyone is thinking the same, the opposite will happen.

Right now, record high dollar volume of trading shows that confidence, at least on this basis, has reached a new historic extreme. (11/09 EWFF)

EWI Chief Market Analyst Steve Hochberg wrote in his Wednesday Short Term Update, "(On Tuesday), the VIX closed back within two standard deviations of its 20-period moving average, which for the past seven months, has resulted in a near-term rally."

On Wednesday, stocks closed up;

Thursday saw a huge rally.

On Friday morning, the Dow regained the 10,000 level. But the Update reports that the "next leg (down)

is fast approaching." (Robert Prechters Stocks Latest Bear Market Update)

We're now in mid-November; the move up from March became the biggest rally in more than five years. Yet the facts are these: Gold is the only commodity to reach an all-time high, the Dow Industrials the only stock index to see a new closing high on the year. A seasoned technical analyst knows this is a classic "non-confirmation" -- and Bob Prechter is a lot more than just seasoned. Here's what he says in his brand-new November 2009 Elliott Wave Theorist: "Only the bluest of the blue chip markets in both the stock and the commodity sectors i.e. the DJIA and gold made significant new highs, while their lesser counterparts have so far all failed to confirm. This type of divergence in trends is the most traditional of all technical conditions warning of distribution." The "experts" apparently think that a few months of financial chaos in late 2008-early 2009 was as bad as it's going to get. They'd have you believe (hope?) that those few months is all it took to reverse a mania that was decades in the making. But our technical indicators aren't based on hope. They give us the facts and the evidence. That's why we ignored the experts in July 2007 and February 2009, and why we ignore them now. Don't allow the recovery hype to put your portfolio at risk. You can read a market forecast that truly is independent. How to Identify the Continuing and Looming Deflationary Forces

...the just-published November 2009 Elliott Wave Financial Forecast sums up what Elliott investors expect next: "This trend reversal also provides an early warning signal that the economic rebound that so many are hailing is near an end." Has the Optimistic Bias of the Past Decade Finally 'Hit the Wall'?

In late November of 2009, Bob Prechter appeared on CNBC to call the top yet again. It's interesting that the "Fast Money" crew largely agrees with his prediction that "we are in for a very large decline in 2010...at least as big as what we saw in '08", which contrasts sharply with his characterization of sentiment as excessively bullish at the time.

WATCH VIDEO:

Prechter then proceeded to recommend a 200% fully leveraged short position to subscribers:

http://www.marketwat...rish-2009-11-25

http://yelnick.typep...l-in-short.html

Here's what the market looked like at the time:

December of 2009 was the first month since August that EWI did not attempt to pick a top in the market. It instead focused on fundamentalist arguments for a pessimistic view of future market activity: What the Government Doesn't Want You to Know and How it Can Hurt You in 2010

In spite of a continued rally, in late December EWI predicted that 2010 would bring a major decline:

Back in the late 1990s, when the "unstoppable" NASDAQ began to experience regular days of double-digit drops, it was "Buy-the-Dip." Now, it's "buy the entire lost decade." And, as the Dec.31, 2009 Elliott Wave Financial Forecast Short Term Update reveals -- current sentiment readings "continue to show that stock market bears have packed up and moved to Florida for the winter."

The Dec. 31 Short Term Update also reveals two mind-blowing charts of the S&P 500 versus Investor Intelligence Advisors Survey Percentage of Bears -- AND, the S&P 500 versus the percentage of "Fully Committed" bullish advisors since 2000. The current reading is the lowest bearish percentage in 22 years.

Take one look at the evidence, and you'll see that a defining pattern emerges: Low levels of bearishness have consistently coincided with one kind of market move. Combine this picture with the other measures of investor sentiment like momentum, volume and Elliott wave structure, and the evidence tilts overwhelmingly in favor of an unforgettable year. (New Year New Economic Boom? Why 2010 Should Be One to Remember)

The market finished the year above all three of Prechter's top calls.

In mid-January, once again, Prechter recommended a 200% fully leveraged short position: http://yelnick.typepad.com/yelnick/2010/01...hort-again.html

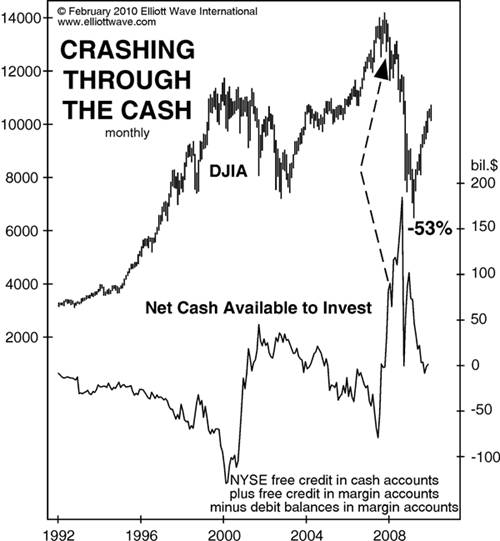

In late January, EWI cited "cash on the sidelines" as an reason for picking a top in the market:

Myth -- Cash on the sidelines is bullish for stocks: This refrain rang like a gong all the way through the declines of 2000-2002 and 2007-2009. In February 2000, when mutual fund cash hit 4.2% (compared to 3.8% in November), The Elliott Wave Financial Forecast issued its cash is king advice. Once again, the word on the street is that there is way too much cash on the sidelines for stocks to fall precipitously. This chart shows net cash available to investors plotted beneath the DJIA. In December 2007, available net cash expanded to a new high, besting all extremes since at least 1992, a 15-year time span. Despite the presence of this mountain of cash, the DJIA lost more than half its entire value over the next 15 months. Indeed, as the chart shows, cash remained high right as the stock market entered the most intense part of the crash in 2008. Available cash does correlate with the markets moves, but the market is in charge, not the cash. --The Elliott Wave Financial Forecast, Jan. 29, 2010

(Stock Market Crashing Through With Cash, Market Myths Exposed)

(Stock Market Crashing Through With Cash, Market Myths Exposed)

In early February, EWI was ebullient as the market had corrected over the course of a three week period:

In case you were hiding out Tiger Woods' style far away from the mainstream media during the past month, let me be the first to say: January saw an abrupt end to the U.S. stock market's record-setting winning streak. Last count, the Dow Jones Industrial Average plummeted 4% in its worst monthly loss in a year.

And, according to one Feb. 1, 2010, MarketWatch story, "The time to consider an exit strategy" has officially arrived. Here, the article captures the public's astonishment turned acceptance of the Dow's boom-to-gloom shift:

"The Dow has shocked the bulls out of their complacency. After all, analysts were looking for the bull market to last until at least the second half of the year. Investors were not prepared for such a sharp decline and now at least some of the chatter has gone from 'how high will the market go?' to 'how low will it fall?'".

Let me get this straight. The powers that be say it's time to "consider an exit strategy" -- AFTER the Dow has already plunged 700-plus points to land at its lowest level in two months. That's about as helpful as building a life raft AFTER your ship has begun to sink.

Then, those same sources go on to say investors were "not prepared" for the degree and depth of the stock market's decline. This is only partly true. On Main Street, the early January flood of bull-is-back-type headlines gushed in and washed all the bears away.

Yet, on our "Elliott wave" Street, preparation for a "sharp" decline in the Dow was fast in place. One week before the market turned down from its Jan. 19 high, Elliott Wave International's Short Term Update went on high bearish alert with this commanding insight:

"The Dow's diagonal remains intact and its form is clear. We will afford the pattern a bit of leeway over the next one-two days... but the structure is very late in development. That means a trend reversal is fast approaching. A potential topping range is 10,725-10,740. A close beneath [critical support] will confirm that the diagonal is over and the market has started a down phase that should draw prices significantly lower. Once a diagonal is complete, prices swiftly retrace to near its origin, which in this case is 10,263.90, the very first downside target." (Jan. 13 Short Term Update)

Soon after, the Dow peaked within four ticks of our cited upside target; next, it went on to fulfill the second part of its Elliott wave script with a staggering triple-digit slide to "near the origin" of the diagonal triangle pattern, and then some.

That leaves one question: Are the bears now ready to relinquish control of stocks? Don't wait for the market action to "shock" you. (U.S. Stocks: Will The Bears Relinquish Control?)

Later in February, EWI turned to a fundamental argument to buttress its predictions of an eventual stock market decline:

Bullish expectations (shown by the top three panels) may not be quite as extreme as they were in 2007, but adjusted for underlying economic conditions (bottom panels), the current psychology probably ranks right up there with the most complacent outlook in history. The charts of housing, consumer credit and unemployment show the systemically sluggish state of the economy. We know that fundamentals always lag psychological trends, but the lag is generally only a matter of months. Its been nearly 11 months since the outset of the Primary wave 2 rally; by these critical economic measures the rebound is barely registering.The wide disparity between the hope of investor expectations and the reality of economic strength shows that the great bear market -- already ten years old -- remains in its early stages. As the next leg down matures, hope will turn to despair, and it will become impossible to ignore the persistence of the economic contraction.

(What Chinese Malls Tell Us about the Economic Reality)

In April of 2010 EWI correctly pointed out a set of conditions which made a market top likely:

It is rare to have technical indicators all lined up on one side of the ledger. They were lined up this way -- on the bullish side -- in late February-early March of 2009. Today they are just as aligned but on the bearish side. Consider this short list:

- The latest report shows only 3.5% cash on average in mutual funds. This figure matches the all-time low, which occurred in July 2007, the month when the Dow Industrials-plus-Transports combination made its all-time high. But wait. The latest report pertains only through February. In March, the market rose virtually every day, so there is little doubt that the percentage of cash in mutual funds is now at an all-time low, lower than in 2000, lower than in 2007! We will know for sure when the next report comes out in early May. Regardless, the confidence that mutual fund managers and investors express today for a continuation of the uptrend rivals their optimism of 2000 and 2007, times of the two most extreme expressions of stock-market optimism ever.

- The 10-day moving average of the CBOE Equity Put/Call Ratio has fallen to 0.45, which means that the volume of trading in calls has been more than twice that in puts. So, investors are interested primarily in betting on further rising prices, not falling prices, and that's bearish. The current reading is less than half the level it was thirteen months ago and its lowest level since the all-time peak of stock market optimism from January 1999 to September 2000, the month that the NYSE Composite Index made its orthodox top. The 30-day average stands at 0.50, the lowest reading since October 2000. It took years of relentless rise following the 1987 crash for investors to get that bullish. This time, it's taken only 13 months.

- The VIX, a measure of volatility based on options premiums, has been sitting at its lowest level since May 2008, when wave (2) of ((1)) peaked out and led to a Dow loss of 50% over the next ten months. Low premiums indicate complacency among options writers. The quants who designed the trading systems that blew up in 2008 generally assumed that low volatility meant that the market was safe, so at such times they would advise hedge funds to raise their leverage multiples. But low volatility is actually the opposite, a warning that things are about to change. The fact that the options market gets things backward is a boon to speculators. Whenever options writers are selling options cheap, the market is likely to move in a big way. Combined with the readings on the Equity Put/Call Ratio, puts right now are a bargain.

- In October 2008 at the bottom of wave 3 of (3) of ((1)), the Investors Intelligence poll of advisors (which has categories of bullish, bearish and neutral), reported that more than half of advisors were bearish. In December 2009, it reported only 15.6% bears. This reading was the lowest percentage since April 1987, 23 years ago! As happens going into every market top, the ratio has moderated a bit, to 18.9% bears. In 1987, the market also rallied four months past the extreme in advisor sentiment. Then it crashed. The bull/bear ratio in October 2008 was 0.4. In the past five months, it has been as high as 3.4.

- The Daily Sentiment Index, a poll conducted by Trade-Futures.com, reports the percentage of traders who are bullish on the S&P. The reading has been registering highs in the 86-92% range ever since last September. Prior to recent months, the last time the DSI saw even a single day's reading at 90% was June 2007. At the March 2009 bottom, only 2% of traders were bullish, so today's readings make quite a contrast in a short period of time.

- The Dow's dividend yield is 2.5%. The only market tops of the past century at which this figure was lower are those of 2000 and 2007, when it was 1.4% and 2.1%, respectively. At the 1929 high, it was 2.9%.

- The price/earnings ratio, using four-quarter trailing real earnings, has improved tremendously, from 122 to 23. But 23 is in the area of the peak levels of P/E throughout the 20th century. Ratios of 6 or 7 occurred at major stock market bottoms during that time. P/E was infinite during the final quarter of 2008, when E was negative. We will see quite a few quarters of infinite P/E from 2010 to 2017.

- The Trading Index (TRIN) is a measure of how much volume it takes to move rising stocks vs. falling stocks on the NYSE. The 30-day moving average of daily closing TRIN readings has been sitting at 0.90, the lowest level since June 2007. This means that it has taken a lot of volume to make rising stocks go up vs. making falling stocks go down over the past 30-plus trading days. It means that buyers of rising stocks are expending more money to get the same result that sellers of declining stocks are getting. Usually long periods of low TRIN exhaust buying power.

One of the most interesting things about the coming decline will be its initial slide down the Slope of Hope. The past ten years have seen an unprecedented sustaining of optimism in the face of deteriorating financial market and monetary conditions and a deteriorating economy. Even though the market is about to begin its greatest decline ever, the era of hope is not quite finished. (04/10 EWT; (Robert Prechter, What Do These 8 Technical Indicators Mean for the Stock Market?)

EWI has presented this same list of indicators at each juncture since August of 2009 (and continues to do so) as representing clear signals that the ultimate top is at hand. I am going to reserve dissection of these data points for the next part in this series, but I will point out that while in part set of conditions has proven to be somewhat useful in identifying intermediate and short term declines within a bull trend, as Prechter himself points out above, but not largely applicable to identifying long term market turns. I also called a top in April of 2010 based on a variety of technical indicators, including many of the same conditions included in EWI's reports, and the completion of a five wave pattern off the March 2010 bottom. And for some time I did hold out the possibility that the bear market had returned. I turned bullish in August following the July bottom and even more bullish at the September bottom.

Prechter presented the following commentary and chart to illustrate the anticipated topping zone for the Dow Jones:

As far as Elliott waves go, the rally since last March is totally normal. Two weeks off the low of March 2009, our Short Term Update published an upside target of Dow 10,000. So we knew a big rally was coming.

The August issue listed the range for typical retracement as being from 9368 to 11,620. This is a wide range, but there is nothing we can do about it; second waves have a lot of leeway. The illustration shown in that issue is reproduced below alongside an update of market prices. The Dow has so far stayed within the normal range."

Even so, I expected the rally to peak in the lower half of the target range then reverse. In August 2009, after 5 months, and in November, after 8 months, I was quite sure that the rally was ending. But instead of stopping near 10,000 at a 50% retracement, it has reached a 60% retracement. (Robert Prechter's Stock Market Trend Forecast 2010 to 2016)

Even so, I expected the rally to peak in the lower half of the target range then reverse. In August 2009, after 5 months, and in November, after 8 months, I was quite sure that the rally was ending. But instead of stopping near 10,000 at a 50% retracement, it has reached a 60% retracement. (Robert Prechter's Stock Market Trend Forecast 2010 to 2016)

I'll briefly point out here that since the proposed right shoulder has now taken out the left shoulder high the probability that this formation will complete and succeed is significantly diminished.

Here's a picture of the market through that date:

EWI proceeded to call "The Top" of the presupposed Wave 2 correction with its next series of reports:

Fibonacci Time Relationships Suggest That the Biggest Stock Market Top Formation of All Time Is Ending in 2010 and That a Price Collapse Will Last Six Years, Until 2016.

Why a Historically Large Collapse Is Likely: Stock-market bulls and most economists think that a new bull market and economic recovery are underway. Most bears are looking for either a long sideways bear market a la 1966-1982 or a hyperinflationary run to infinity. Our Elliott wave outlook opposes both of these scenarios. The most likely profile is a stock market crash of historic proportions. There are a number of reasons why the Dow should decline into three digit territory...

Obviously, this outlook is extreme beyond all investors present imagining. But consider how these socionomic expectations combine to indicate much lower prices: Downward adjustments in stock-market valuations by 60%, corporate worth by 80% and the dollar-based credit supply by 80%all at the same timewould produce an overall stock-price decline of 98-99%. I consider a forecast of a 92% decline or morei.e. calling for a triple-digit Dowto be conservative.

One of the most interesting things about the coming decline will be its initial slide down the Slope of Hope. The past ten years have seen an unprecedented sustaining of optimism in the face of deteriorating financial market and monetary conditions and a deteriorating economy. Even though the market is about to begin its greatest decline ever, the era of hope is not quite finished.

Second waves rekindle optimism. Recall the environment after the peak of October 2007. The stock market slipped for a month and then rallied in Minor wave 2 into December; the consensus called for new highs...The decline that begins in 2010 will proceed along similar lines. But this time the entire decline will last four times as long as the 17 months of wave 1, so the entire process of dashed hopes will take longer. The fall will also be much deeper, so it will be impressive to watch how tenaciously investors, government and the Fed cling to hopes despite the markets continual falls to new lows. The era of hope will end when the last second wave is over and the last cycle has topped, just before the center of the declining structure. (05/10 EWT)

...the Dow does not yet sport five waves down at Intermediate degree. So, the wave pattern has yet to confirm a new downtrend. But two things strongly suggest that a new wave of bear market is in force. First, volume continues to expand on declines and contract on rallies. Second, volatility has soared since the markets peak. These two conditions attend bear markets way more often than bull markets. We therefore maintain our opinion that the April 26 high was the end of the bear market rally that started in March 2009. (06/10 EWT)

The April 16, 2010 issue of The Elliott Wave Theorist, titled A Deadly Bearish Big Picture, provided our roadmap for the next half dozen years in the stock market. Stocks are down from that point, yet as the companion issue of May 8 predicted, financial commentary has remained steadfastly bullish. The majority has hailed every rally since April as marking the resumption of a bull market. Following a gentlemanly article in the New York Times on July 4, my call for a serious resumption of the bear market is being dismissed and ridiculed in the press. This is the way it should be because social mood, which regulates general stock market opinion, is once again historically elevated.

As for the short term outlook, the stock market rallies of June and July have the earmarks of a wave 2", implying that a powerful wave 3 down lies directly ahead. Even if it doesnt happen right away, it will occur eventually, so we are maintaining our stance of extreme safety and waiting for the market to issue its verdict. (07/10 EWT)

In August, as the uptrend resumed and made its first high, EWI again called for a resumption of the bear market:

The stock market has been in an upward correction for over two months. Evidence is quite strong that the rally is over. The July-August rally is taking a wedge shape, especially in the S&P and NASDAQ. Wedge shapes are usually terminal. Times when they are not are resolved with huge breadth and volume in a continuation of the trend. A surge of that type is the only thing that can rescue this market from a downside reversal. The latest stock market rallies have the earmarks of a "wave 2", implying that a powerful "wave 3" likes directly ahead. (08/10/10 EWT Interim Update

)In September, as the market made a higher low and accelerated to the upside, EWI signaled a "resumption of the downtrend":

Every short-term upward stab in stocks keeps investors hoping that the bear market is finally over. It is not. The larger downtrend returned back in late April, and stocks are setting up for a powerful leg lower...The DJIAs worst August in nine years (-4.3%) should signal the resumption of the downtrend that began in April, as The Elliott Wave Financial Forecast called for a month ago. As we also pointed out last month, August can be a big month for trend changes. We were specifically referring to a long line of stock market reversals discussed in EWT and EWFF. As the Dow now abandons the territory traversed through this 13-year topping process, the last vestiges of extreme optimism produced by the Great Bull Market will be wrung out and a dramatic bear market alteration of the social order will pick up speed.

On a shorter term basis, the stock market completed the right shoulder of an eight month-long head-and-shoulders topping pattern on August 9 when the DJIA pushed to 10,720, essentially matching the termination level of the left shoulder at 10,730 on January 19. A close beneath the down-sloping neckline at 9500 will confirm the completion of the pattern and target the area near 8000 for a measured move. Eventually, the March 6, 2009 low of 6470, the low point within the entire 13-year top shown on the upper chart, will fall in conjunction with a significant spike in volatility.

The August 9 high 10,720 in the Dow and 1129 in the S&P marks the top of Minor wave 2, which traced out an upward expanded flat labeled a-b-c. Wave c formed a wedge, which is classic ending pattern. Observe the waning upside momentum in the rise to this high, as depicted by the contracting daily NYSE volume, another attribute of terminating wave....With stocks still descending in a long-term bear market, interest in stock trading has waned, as seen in the dearth of daily trading volume on the NYSE. By some estimates, it is at an 11-year low.

In summary, the evidence is strong that the bear markets next leg down is underway. (09/10 EWFF)

On April 16, 2010, at the peak of the new orgy of stock market optimism, EWT issued an in-depth study of cycles, waves, technical patterns and indicators titled A Deadly Bearish Big Picture. Ten days later, the market peaked...The sideways market of the past four months has been well within our description of how things would play out. The second-wave rally is rekindling optimism...Optimism will remain investors default mood during this entire time. We expected a stair-step decline from the April high and said that every rally through at least 2011 and maybe 2012 would be greeted as the resumption of a bull market. This is exactly whats been happening...The April high in the S&P was 1220. On the day of the flash crash, which was May 6, the S&P closed at 1128. It has not closed above even that level for a single day in the four months since May 17. Yet optimism remains dominant...One indicator of slackening momentum during this time does have implications about the future: the volume pattern. Volume has diminished on the rallies this summer, and it has especially retreated during the September rally to date. This tells you that upside momentum, despite investors optimism, is terrible. The market has been attracting volume when it falls but not when it rises...the markets rallies since the April high are counter-trend moves. (09/10 EWT)

WATCH VIDEO: CNBCSept. 27, 2010--Robert Prechter, president of Elliott Wave International, tells CNBC he's extremely bearish on the market and expects the Dow to fall below 1,000 within the next six years.

At this time 3 out the 5 EWI top calls were in the red:

EWI incorrectly called a C wave top in October 2010, suggesting that a complex "double three" pattern had completed:

The set up is very strong for the start of an across-the-board decline in most markets. Several important wave relationships indicate that a return to the larger downtrend is imminent...An across-the-board optimistic extreme over the past four months has lifted stocks, the euro, commodities and precious metals. This rise is almost certainly ending as we go to press. The stock market is on the cusp of completing a second wave rally high, having partially retraced the decline that started in April. A definitive wave structure suggests that the next leg of the ongoing bear market is at hand.

A time correspondence within wave Y makes the case for a top even stronger...if wave 2 up concludes during this time period, the last upward zigzag of the correction will feature a low-to low equals high-to-high time relationship as well as a low-to-high time correspondence between the two rally legs. Thus, pattern, price and time have converged to make a case that the start of wave 3 down is imminent. (10/10 EWFF)

The September issue reiterated that optimism will remain dominant for another two years even though markets will be resuming bear trends. This month, optimism has become too extreme to sustain. Elliott waves combined with sentiment measures indicate some imminent turns...The Elliott Wave Financial Forecast made the case that Minor wave 2 in the stock market is ending. Overall breadth today was again very narrow, and the NASDAQ may have completed an ending diagonal at todays close. Minor wave 3 should carry the S&P down about 400 points over the next few months. A drop of that magnitude would close the chapter on the Right Shoulder of the great Dow top. (10/10 EWT)

Strategy update: The only bullish chart in the financial pantheon is that for the U.S. dollar. Investors should avoid everything else. Traders should stay short the S&P and sell short the euro. If you are a speculator who joined us after January 2010 and are not already short the stock market, use this opportunity to take a maximum leveraged short position. If you want to take a flyer shorting precious metals or certain commodities, our Metals and Commodities Special Services track these markets daily. (10/10 EWT)

MarketWatch.com's Mark Hulbert noted that Prechter recommeded "that traders allocate 200% of their stock trading portfolios to shorting the stock market" and commented that "this helps to explain why the newsletter's timing advice for traders is in last place for performance over the last 20 years among all stock market timing strategies tracked by the Hulbert Financial Digest."In November, EWI called the top yet again:

Stocks continued to rally through October, carrying the blue chip indexes above the April highs. In doing so, however, several measures of investor sentiment hit optimistic extremes that exceed those recorded at the October 2007 all-time Dow high. Yet, the Dow and S&P each remain well beneath their respective 2007 peaks, providing a potentially potent reversal signal...Stocks are near the end of the rise from at least late August. Technical conditions are about as ripe for this turn as they were in late 2007...Instead of resuming the larger bear market last month, as we presumed, stocks continued their upward push. The DJIAs rise past its April high at 11,258 means that Primary wave 2 is still unfolding. The rally from March 2009 to April 2010 was wave (A); the decline to 9614 in July was wave ( and the rise since this low is wave ©. A complete (A)-(-© will mark the top of 2...A new multi-year high in investor optimism is occurring even as the internal strength of the markets push is lagging. For instance, the 10-day average of the NYSE advance/decline ratio and the 10-day NYSE up/down volume ratio...made their respective countertrend rally highs on September 15. Despite the new Dow recovery high, each oscillator has so far remained beneath its September high.... These measures taken together paint a clear picture: fewer stocks are participating in the rally, which often occurs prior to a trend reversal. These conditions do not indicate that one should be buying the market. They indicate exactly the opposite: that one should be focusing intently on an impending change of trend from up to down. (11/10 EWFF)

and the rise since this low is wave ©. A complete (A)-(-© will mark the top of 2...A new multi-year high in investor optimism is occurring even as the internal strength of the markets push is lagging. For instance, the 10-day average of the NYSE advance/decline ratio and the 10-day NYSE up/down volume ratio...made their respective countertrend rally highs on September 15. Despite the new Dow recovery high, each oscillator has so far remained beneath its September high.... These measures taken together paint a clear picture: fewer stocks are participating in the rally, which often occurs prior to a trend reversal. These conditions do not indicate that one should be buying the market. They indicate exactly the opposite: that one should be focusing intently on an impending change of trend from up to down. (11/10 EWFF)

In April, the Dow Industrial Average reached a 61.8% retracement of the 2007-009 decline on an intraday basis, and we were sure that was it. The S&P at the time achieved only a 60.8% retracement. The Dow has now traveled to a 64.5% retracement intraday (64.3% using daily closes), while the S&P 500 index has reached a 61.8% retracement on daily closing basis....The best wave count, as shown in the October EWFF, labels the recent high as wave 3 of ©, indicating one more high of Minor degree to come. Within the double top of 2007, the technical condition of the market was notably worse at the second peak thant the first. This year, the technical condition is more bearish in November than it was in April. Upside momentum is far less now than in April, as evidenced by the lower 10-day a/d and upside/downside volume ratios. At the same time, sentiment has crystallized to extreme bullishness. In April, we figured that the highest percentages of bulls since the all-time high of October 2007 was enough for the end of Primary wave 2. Apparently not. In November, the Daily Sentiment Index for S&P traders reached 94% bulls, and the American Association of Individual Investors poll reached 57.6% bulls. Both readings are the highest since January 2007, nearly four years ago. Investors Intelligence just reported 56.2% bulls, the highest level since the 56.5% of December 2007. Investors have swallowed the omnipotent Fed argument, and it shows. Perhaps this condition (along with GMs near-record IPO) is fitting for the peak of the right shoulder of the biggest head & shoulders pattern ever formed. As far as Im concerned, nothing has changed except for the worse. The stock market is a terrible value and a technical disaster, and it has been at all three tops this year. The Feds QE2 announcement will probably prove to be one of the most expensive buy signals of all time. Stay liquid. (11/10 EWT)

In December, EWI seemed a bit desperate to defend its crumbling credibility, looking to Wikileaks, junk bonds and sovereign debt to spark the predicted collapse:

A top in stocks may not be in place just yet, but the credit/liquidity crisis that roiled financial markets beginning in late 2007 is re-asserting itself. This alignment suggests that the next phase of the bear market will encompass nearly all freely traded markets, just as it ultimately did in 2008. For stocks, the rallys end should come after one more new recovery high. The backdrop of multi-year, optimistic extremes in various sentiment measures is already in place. The fear of default on junk debt has waned to a level that also indicates the start of the downturn is rapidly approaching.

In October 2007...The Elliott Wave Financial Forecast cited the critical importance of the forecasted credit contraction, which was very much in evidence, at that time. Liquidity is clearly drying up as confidence wanes and a steady movement toward an across-the-board decline is happening, stated EWFF. November 2010 represents a larger version of the same scenario. Fears of default are once again mounting, in the same manner. The current threat moved from Greece in the early part of 2010 to Ireland, as the Dow pushed to a November 5 high. Last week, the debt fear spread rapidly to Portugal, Spain and Italy. According to the latest accounts, it is now moving from the euro-zone periphery to the core, with Belgium coming under the most pressure followed by France.

The best wave formation indicates that stocks are tracing out Minor wave 4, which started at the November 5 highs. Since wave 2 was a sharp pullback, the guideline of alternation indicates that wave 4 should be a sideways correction. A triangle or flat, both members of the sideways family of corrections, would fulfill the guideline. In both near-term scenarios, wave b of 4 is complete, or very nearly so.

The big takedown will come in 2011 when Julian Assange, the publisher of secret documents through his website Wikileaks.org, says he will turn his attention to Wall Street. He compares Wikileaks next Megaleak to the damning e-mails that poured out of the Enron trial, as stocks slipped lower in 2001 and 2002.

Of course, the emerging bear market in mood is huge, so its not as if the media needs evidence. On November 22, The New York Times was already asking, Can Wall Street Justify Its Existence? A subsequent New Yorker headline seemed to answer: Much of What Investment Bankers Do Is Socially Worthless.

After years of social adulation, it will only take an incremental reduction in risk assumption to tip the scales against the markets.

Our view remains that this environment is perfect for eliminating any and all junk debt from ones portfolio, as deflation will ravage everything but the highest quality bonds. The torpedoing of European sovereign debt and the biggest monthly drop of the year for U.S. tax exempt municipal bonds means that the trend toward increasing distress is probably already underway. (12/10 EWFF)

To summarize the situation, the technical condition of the stock market is compatible with an approaching resumption of the Supercycle-degree bear market under the Elliott wave model. By definition most other traders, investors, advisors, money managers and economists view a bearish outcome as remote. Sentiment is crystallizing so strongly that economists and market strategists have rushed to raise their estimates for 2011...Since December, despite continuing new highs in the S&P, new highs on the NYSE have continued to slip...The entire picture is one of lessening upside momentum over the past eight months, five weeks and one week...I have been warning for a long time that there will be a panic into cash before this bear market is over. Even though investors are intensely bullish on stocks, precious metals, commodities and junk bonds, there has nevertheless been a stealth move toward holding cash. (12/10 EWT)

WATCH VIDEO: Bob Prechter on CNBC, December 30, 2010: "Not a bear among them"

The New Year did nothing to dampen EWI's enthusiasm for a disastrous future. Once again, they called a top:

Can you feel the excitement toward stocks as 2011 arrives? Its palpable. This sentiment extreme combined with a complete wave structure places the stock market on the cusp of a major decline. Theres a good chance the New Year will start with a bang across the breadth of the financial markets. Check out this front page headline from the December 17 USA Today. According to the story, Five Wall Street heavyweights say its time for individual investors to get over their fear of the U.S. stock market. Follow-up headlines in the Money section added: In 2011, Its All About Stocks and 5 Top Experts Agree: New Years Looking Great for Stocks.

It seems that not a single major money manager interviewed by the financial press is telling people that 2011 will be a down year

Lets be clear: These firms and individuals are highly talented and successful. But a crowd is a crowd, no matter how much talentnd money it may possess. When opinion becomes so lopsided that there is not a bear among them, it almost always pays to take the other side of that stance...High % bullish readings (i.e. 90% or higher) suggest that a short-term top is developing or has been made. Low % bullish readings (i.e. 10% or lower) suggest that a short term bottom is developing or has been made...Last months Bottom Line said, The rallys end should come after one more recovery high. That push is mostly played out as we go to press; when complete, it should lead to a historic downside reversal. Minor wave 5 of Intermediate wave © started on November 9 at 10,929.30 in the DJIA. Fifth waves are ending waves, which means that wave 5 will complete the rally from 9614.30, the July low. And the end of the advance from July will mark the top of wave 2, the entire Primary-degree bear market rally that began in March 2009. A top of this magnitude would be entirely consistent with the multi-year extremes in sentiment and the waning upside momentum. (01/11 EWFF)

2011 Should Be a Down Year Across the Board: On the heels of record optimism in two dozen markets, the year 2011 is setting up to be a down year in every popular investment. ..Cash should outperform virtually everything...the NASDAQ 100 should soon begin tracing out wave c down, which will bring it substantially below its 2002 low of 95.25...I suspect that the Dow will fall back below the 2/3 retracement level with just as much enthusiasm as it showed in getting above it. Second waves can retrace 99% of first waves, but they usually dont, and at this point Im out of expected levels...Despite the markets tendency to stretch on the upside, the great Head & Shoulders top formation in the DJIA dating from 2000 has so far managed to maintain its structure. Because it has a down-sloping necklinei.e. the 2009 low is below the 2002 lowI expected a lower peak on the right shoulder. The high reading on the left shoulder in January 2000 is 11,750, and the high reading so far, on January 5, is 11,743. If that day marks the high of the right shoulder, the market went as far as it could without skewing the normal shape of the pattern...The last time the Dow ended an Elliott wave of Primary degree on the cusp of the year was 1976, 34% years ago. Then Primary wave 1 topped on December 31; this time Primary wave 2 may have topped on January 5. (01/11 EWT)

While stocks have extended their push, the structure of the rise appears to be a clear Elliott wave that is terminal. When the bear market resumes...our analysis leads us to conclude even more strongly now than in 2007 that a powerful across-the-board decline will be the next major financial event. Here again, the Wave Principle and historically high optimism are the primary reasons. After impulse waves down ended in December 2008 through March 2009, world stock indexes as well as commodities, oil and many financial markets have rallied in a synchronized (A)-( -© pattern that is the hallmark of an Elliott wave correction. 2011 should see a resumption of the bear market and the beginning of another crushing deflation that will sweep across all of these markets...The blue-chip stock indexes continued higher through January. Overall, measures of the markets breadth and upward momentum remain consistent with the wave interpretation shown on the weekly S&P chart. Tuesdays NYSE advance/decline ratio was strong at 4.6:1, but there was no follow-through, as breadth was negative the next day. Moreover, this weeks new recovery high in the Dow Industrials was not confirmed by the Dow Transportation Average, which made its closing high on January 13, thereby intensifying a bearish Dow Theory non-confirmation. These events are compatible with a rally that appears terminal...Now, some readers ask why we wont simply turn bullish on stocks again since Primary wave 2 has surpassed the targets EWFF set for the rally in April 2009. After all, this is what many others are doing. In our experience, these questions tend to intensify near market highs when we are too far ahead of an important turn. Similar critiques hit EWIs email inbox in 2007, as the Dow Transports and many secondary indexes were topping out in July. The blue chips held up until October, but the ensuing decline into the first quarter of 2009 turned out to be historic. We should have done a better job of honing in on the start of the turn, but, as the intensity of the decline in 2008 showed, its critically important to be safely out of the way of this bear market. (02/11 EWFF)

-© pattern that is the hallmark of an Elliott wave correction. 2011 should see a resumption of the bear market and the beginning of another crushing deflation that will sweep across all of these markets...The blue-chip stock indexes continued higher through January. Overall, measures of the markets breadth and upward momentum remain consistent with the wave interpretation shown on the weekly S&P chart. Tuesdays NYSE advance/decline ratio was strong at 4.6:1, but there was no follow-through, as breadth was negative the next day. Moreover, this weeks new recovery high in the Dow Industrials was not confirmed by the Dow Transportation Average, which made its closing high on January 13, thereby intensifying a bearish Dow Theory non-confirmation. These events are compatible with a rally that appears terminal...Now, some readers ask why we wont simply turn bullish on stocks again since Primary wave 2 has surpassed the targets EWFF set for the rally in April 2009. After all, this is what many others are doing. In our experience, these questions tend to intensify near market highs when we are too far ahead of an important turn. Similar critiques hit EWIs email inbox in 2007, as the Dow Transports and many secondary indexes were topping out in July. The blue chips held up until October, but the ensuing decline into the first quarter of 2009 turned out to be historic. We should have done a better job of honing in on the start of the turn, but, as the intensity of the decline in 2008 showed, its critically important to be safely out of the way of this bear market. (02/11 EWFF)

CONCLUSIONS

Here I will try to examine just a few of the problems of trading methodology which have contributed to the disastrous performance of EWI during the period under review.

TRADING DISCIPLINE AND STOP LOSSES: EWI appears to exercise an astounding lack of trading discipline. At no point does EWI instruct its followers on stops, stop levels or alternate scenarios which would call its bearish assumptions into question. This defies the most basic, elementary, generally accepted rules of trading and risk management. EWI assumes that it will eventually be correct due to an infallible "analysis" and that all will eventually be made right and whole when "The Big One" hits the markets. This is quite simply the mentality of the amateur speculator. Having said this, I will reiterate: Indeed, in the final analysis all bearish errors in analysis and timing may be forgiven when and if the markets do go into a deflationary bear market. This is a possibility. It is however not the current message of the market and the mere possibility of an eventual bear market does not absolve the analyst and the trader from maintaining discipline. Not even the great Jesse Livermore himself could defy the rules of risk and money management. It was his failure to keep fast to his own trading principles in this regard which led to his ultimate demise and suicide.

In "Elliott Wave Principle", Robert Prechter discusses the risks of falling into subjective analysis:

Bolton used to say that one of the hardest things he had to learn was to believe what he saw. If the analyst does not believe what he sees, he is likely to read into his analysis what he thinks should be there for some other reason. At this point, his count becomes subjective. Subjective analysis is dangerous and destroys the value of any market approach.

What the Wave Principle provides is an objective means of assessing the relative probabilities of possible future paths for the market. At any time, two or more valid wave interpretations are usually acceptable by the rules of the Wave Principle. The rules are highly specific and keep the number of valid alternatives to a minimum. Among the valid alternatives, the analyst will generally regard as preferred the interpretation that satisfies the largest number of guidelines, and so on. As a result, competent analysts applying the rules and guidelines of the Wave Principle objectively should usually agree on the order of probabilities for various possible outcomes at any particular time. That order can usually be stated with certainty. Let no one assume, however, that certainty about the order of probabilities is the same as certainty about one specific outcome. Under only the rarest of circumstances does the analyst ever know exactly what the market is going to do. One must understand and accept that even an approach that can identify high odds for a fairly specific outcome will be wrong some of the time. (p.42)

Some may claim that EWI's real position is the safety of cash, but as I have documented here they have clearly advocated 200% leveraged short positions on at least three occasions and have clearly called "The Top" on at least 8. When a top or bottom is clearly called it is also a call to take a position in the direction of the call. There is no evidence that they ever called for those positions to be stopped out; in fact the most recent EWFF maintains a long standing Primary and Intermediate short call. The "safety of cash" defense does not wash.

TOP PICKING: EWI also consistently engages in one of the most amateur of all trading practices: top picking. This selection from the Wall Street classic "Reminiscences of a Stock Operator" illustrates Jesse Livermore's painful experience with top picking:

I was nearly twenty-seven years old. I had been at the game twelve years. But the first time I traded because of a crisis that was still to come I found that I had been using a telescope. Between my first glimpse of the storm cloud and the time for cashing in on the big break the stretch was evidently so much greater than I had thought that I began to wonder whether I really saw what I thought I saw so clearly. We had had many warnings and sensational ascensions in call-money rates. Still some of the great financiers talked hopefully at least to newspaper reporters and the ensuing rallies in the stock market gave the lie to the calamity howlers. Was I fundamentally wrong in being bearish or merely temporarily wrong in having begun to sell short too soon? I decided that I began too soon, but that I really couldn't help it. Then the market began to sell off. That was my opportunity. I sold all I could, and then stocks rallied again, to quite a high level.

It cleaned me out.

There I was right and busted!

I tell you it was remarkable. What happened was this: I looked ahead and saw a big pile of dollars. Out of it stuck a sign. It had "Help yourself," on it, in huge letters. Beside it stood a cart with "Lawrence Livingston Trucking Corporation" painted on its side. I had a brand-new shovel in my hand. There was not another soul in sight, so I had no competition in the gold-shoveling, which is one beauty of seeing the dollar-heap ahead of others. The people who might have seen it if they had stopped to look were just then looking at baseball games instead, or motoring or buying houses to be paid for with the very dollars that I saw. That was the first time that I had seen big money ahead, and I naturally started toward it on the run. Before I could reach the dollar-pile my wind went back on me and I fell to the ground. The pile of dollars was still there, but I had lost the shovel, and the wagon was gone. So much for sprinting too soon! I was too eager to prove to myself that I had seen real dollars and not a mirage. I saw, and knew that I saw. Thinking about the reward for my excellent sight kept me from considering the distance to the dollar-heap. I should have walked and not sprinted. That is what happened. I didn't wait to determine whether or not the time was right for plunging on the bear side. On the one occasion when I should have invoked the aid of my tape-reading I didn't do it. That is how I came to learn that even when one is properly bearish at the very beginning of a bear market it is well not to begin selling in bulk until there is no danger of the engine back-firing.

Let's consult "Elliott Wave Principle" on this matter:

Most other approaches to market analysis, whether fundamental, technical or cyclical, have no good way of forcing a change of opinion if you are wrong. The Wave Principle, in contrast, provides a built-in objective method for changing your mind. Since Elliott Wave analysis is based upon price patterns, a pattern identified as having been completed is either over or it isn't. If the market changes direction, the analyst has caught the turn. If the market moves beyond what the apparently completed pattern allows, the conclusion is wrong, and any funds at risk can be reclaimed immediately. Investors using the Wave Principle can prepare themselves psychologically for such outcomes through the continual updating of the second best interpretation, sometimes called the "alternate count." Because applying the Wave Principle is an exercise in probability, the ongoing maintenance of alternative wave counts is an essential part of investing with it. In the event that the market violates the expected scenario, the alternate count immediately becomes the investor's new preferred count.Of course, there are often times when, despite a rigorous analysis, the question may arise as to how a developing move is to be counted, or perhaps classified as to degree. When there is no clearly preferred interpretation, the analyst must wait until the count resolves itself, in other words, to "sweep it under the rug until the air clears," as Bolton suggested. Almost always, subsequent moves will clarify the status of previous waves by revealing their position in the pattern of the next higher degree. When subsequent waves clarify the picture, the probability that a turning point is at hand can suddenly and excitingly rise to nearly 100%.

Of the many approaches to stock market analysis, the Elliott Wave Principle, in our view, offers the best tool for identifying market turns as they are approached. If you keep an hourly chart, the fifth of the fifth of the fifth in a primary trend alerts you within hours of a major change in direction by the market. It is a thrilling experience to pinpoint a turn, and the Wave Principle is the only approach that can occasionally provide the opportunity to do so. Elliott may not be the perfect formulation since the stock market is part of life and no formula can enclose it or express it completely. (pp.42-43)

A minimum confirmation would be a trend line break. A second confirmation might be a retest of the trend line break and a lower high. Another, more significant confirmation would be a five wave move against the prior trend followed by a three wave move back to retrace a significant portion of the first move for a lower high. This would be the trader's entry point for the new, prospective trend. The prior high would provide the stop loss point. This is not rocket science. It is really Trading 101. Robert Prechter and Elliott Wave International have picked a top on at least eight occasions since March 2009 and completely ignored these basics with negative consequence.

At the April 2010 top I was aware that a five wave advance was coming to its end. There were a number of technical indicators which suggested a substantial correction was due. These two factors led me to exit my long positions on strength in April and begin looking for an opportunity to turn intermediate term bearish. On a trendline break, I sold short. Now, my alternate bearish count told me that there was some possibility that the bear market would resume and so I began to consider my short position as potentially seed money for a much longer term move. For a variety of reasons I turned bullish again in August and even more bullish in September. I still maintain an alternate bearish count which is essentially the same as the EWI count.

Let's assume, for the sake of argument, that I approached the April 2010 top with a primary bearish count and based on that EW analysis I was preparing for a major top and trend change. How might I have approached that in a way which would have maintained trading discipline and preserved capital? Let's look at a chart:

In January 2010 I might have sold short the apparent C wave rising wedge on a break of the lower rail of the uptrend (in fact I did, but only as an intermediate term play). I might have covered that short position when the three wave move from the top failed to produce a five wave bearish impulsive decline or I might have covered at the breakeven point (indicated by the first green arrow). Still confident in my bearish analysis, I might have concluded that a trendline break and break from a topping pattern in April would be a good shorting opportunity (indeed I did sell that break short as indicated earlier). I might have concluded that the August high was an opportunity to add to my short position as a potential Wave 2 corrected 50% of the Wave 1 decline. When that decline failed to produce a bearish impulsive five wave move down I might have covered the August short on the trendline break or at the breakeven point. Finally, I would have covered the April short at breakeven in November. On the second penetration of the April high in December, I might have gone long since the trade setup had failed. I would have been proven wrong in my position by the market but would have lost only time and opportunity and no capital. This is the difference between the use of basic trade and risk management and top picking with no stops.

For the sake of comparison, here is a chart of my BullBear Trading SPX trading calls for 2010:

During most of this period there were far more entries and exits than I would have liked but, given the extreme volatility and that for a time the direction of the trend was in doubt, I shifted to an intermediate and short term trading orientation until the September bottom.

INTELLECTUAL HUBRIS: The kind of performance documented here becomes possible when a trader or analyst turns the market into an ego driven intellectual exercise. Market analysis is not a game to prove that you are smarter than the rest of the pack or smarter than the market itself. I find Prechter's commentary and promotional propaganda saturated with entirely unwarranted egoic smugness that can only be compromising to the goal of staying on the right side of the markets. It's that sort of mentalilty which underlies and creates the psychological potential for a lack of trading discipline and a consistent practice of top picking.

In coming installments of this series I will analyze the data and the methodology utilized by Elliott Wave International in the process of its trading history from March 2009 to present.

Need some help staying on the right side of the markets? Join the BullBear Trading room at TheBullBear.com. You'll get this kind of timely, incisive, unbiased stock and financial market trading and investment technical analysis and commentary daily. It's free to join, no credit card is required and if you like my work you just make a donation at the end of each month.

http://api.ning.com:80/files/YXPKNxMJR7*N5...no&type=pnghttp://api.ning.com:...5...no&type=png

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}