|

Gene Inger's Daily Briefing (highlights) - for Thursday, March 16, 2017

|

|

Prepping for a rally testing the highs - for over a week, as we signaled a healthy market consolidation just waiting to get past the Fed's universally expected rate hike (the variance being: I was confident of a favorable S&P response). There was a reasonable satisfaction at behavior which technical analysis had envisioned moving up, based on preceding internal rotation.

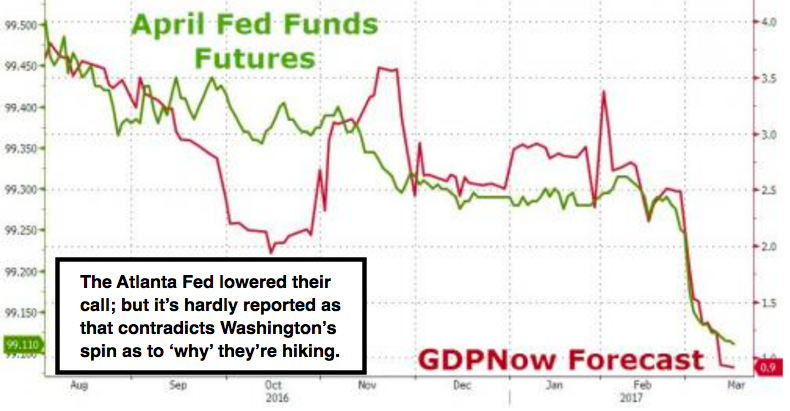

Yes, Chair Yellen not putting her finger on a 'hair trigger' quite aggressively (language about the 'pace' of hikes) is the common explanation. However it was pretty clear the Fed is prepared for additional hikes as 'accommodation' becomes less justifiable (rates at essentially artificially low levels) should we actually get the kind of economic strength they essentially 'spin' for now.  The 'spin' is because they're already behind the Curve to a degree; because inflation is evolving while economic activity is generally sluggish (details). At the same time, the stock market had remained strong outside of Oil; so I warned NOT to short Oil; but looked for it to kick-in with a rebound. And no problem getting the NASDAQ to new highs; initiating a secondary test of the S&P 2400 plus preceding highs after another forecast rally; that being one expected if Trump called for 'unity' at the big speech which he did; trapping moaning bears yet-again. Totally bullish for near 5 months now, since the middle of Election Night, without even a trading fade; no shorting; and no selling of stocks.  Now, no doubt there's a 'real' (redacted) coming and short-interest is lower, as I noted last evening. Meanwhile we run-in shorts that are out there after warning against shorting and against bearish option strategies; continuously since just before Election Day; when I opined few would believe how bullish I'd be if 'The Donald' carried the day. It's not about political partisanship; it's about bringing the Country back and markets confirmed we were right. Most did not embrace the move's rotational nature we persistently talked of in early November; and that was shifts into old cyclical and basic industrial stocks that were dormant for years, or in 'bear markets' of their own. Many money managers failed, or reluctantly climbed-onto the market bandwagon, and had trouble adjusting portfolios quickly, so as to reflect the new reality. That means that they are (this part is reserved for subscribers; please join).  Is President Trump doing everything right? Nope. Is the media continuing to unfairly address some subjects, or 'work them into' a dialogue that clearly is trying to sway viewers by implicitly leaning toward bias? Sure. Is there risk a real scandal erupts from rising circumstantial inferences (if not real factual evidence), that has an impact on the markets as some point. Yes. However, while holding longs from the lows and not chasing strength; we calmly have sailed through the 'Ides of March' and suspected the modern Brutus(es) out there would not bring down the market by their vitriolic pleading for decline. Bottom-line: we forewarned traders NOT to short or fade this market even as we anticipated a pullback after the Speech to Congress. And during the consolidation we called for preparation to spur the market to a test of highs immediately in the wake of the Fed's decision; expected to be what it was. Along the way, we considered the markets quite stable absent Oil doing well and suggested Oil should rebound (too many crowded shorts in recent days as mentioned again yesterday) even if the overall heaviness returns later. Tonight we'll do a brief update of LightPath Technologies (LPTH) below, and note we're going right into a (Quarterly) Expiration finale. Tonight's video will indicate how I think it's likely going to unfold into next week's action. |

|

|

|

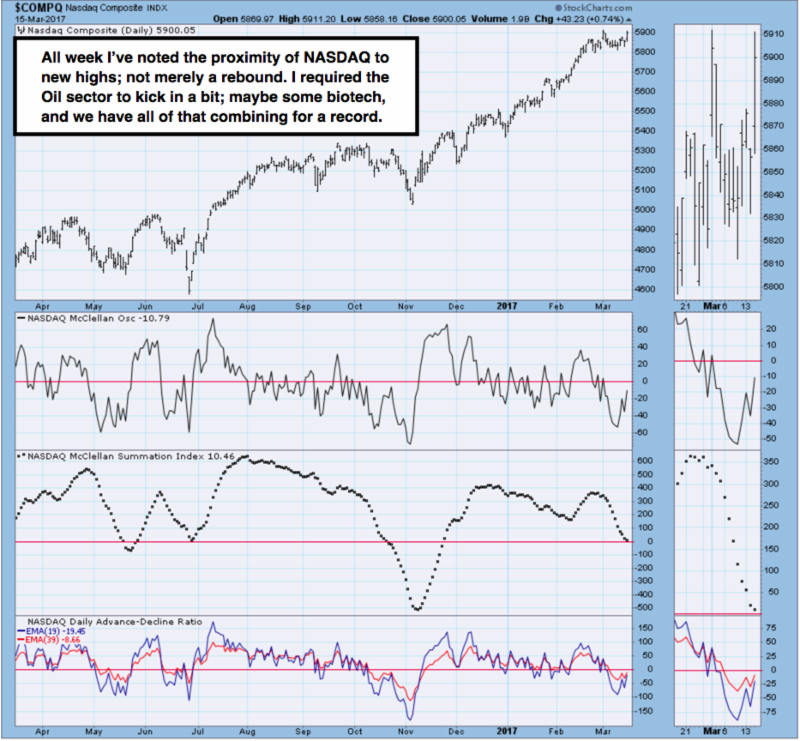

Daily action - remained quite stable even when on the defensive earlier this week; as the market prepared to rally (in our view) after the Fed hiked rates.

Technically the market (ironically) had been retreating... but it was internal. That is why you saw the breadth indicators (including the Oscillators) easing for weeks, but failing to drag the entire market down with it.. consolidation or a mild correction only; on a rotational basis between stocks and sectors.

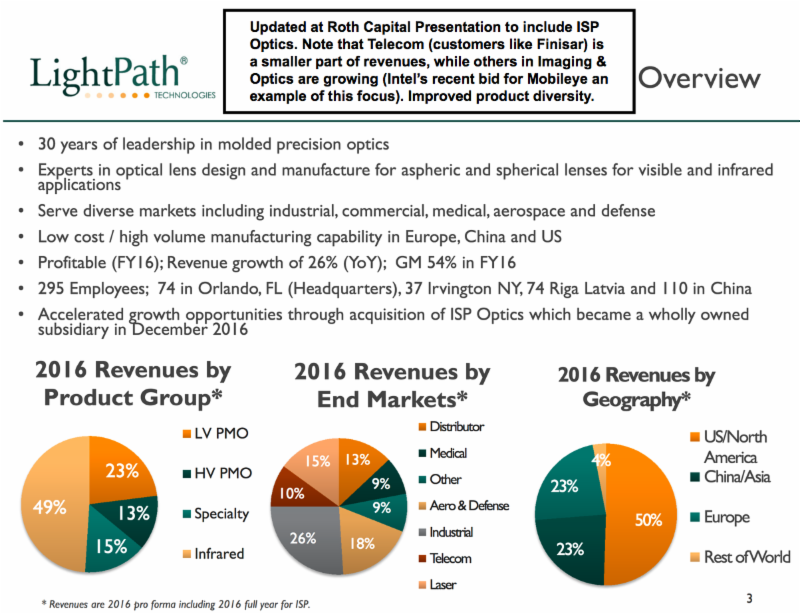

Notice we allowed for consolidation; pointed to relative strength of NASDAQ during all of this; and opined that this technically left the Averages in a great position to thrust towards the highs after the Fed's decision on rates (which I discuss in the second video), which I thought was right on the money.  We've had a chance to look over the LightPath (LPTH) 'Presentation charts' at this week's Roth Capital institutional gathering. I'll share the overview and a couple updated slides, as their financials point to a continued growth path within optics, now combined with infrared production (ongoing integration of Europe's ISP Optics thermal imaging with LPTH's optical business). (This was our 2017 'speculative pick with a 1.40-1.60 buy zone; and a target above current levels for the intermediate term.) If it eventually moves above 5, that's when institutions may increase interest, as many are not allowed to hold positions in stocks below 5, other than from an Index participation. The growth rate and product diversity are improved, and we'll see how well their foray into autonomous driving goes as well. Speculative but looks solid. I'll continue to update this stock regularly as promised. (So far it's about 50% ahead in the two months since the initial write-up for our subscribers.)     What you see are a few new customers I don't recall, plus Israel's Ministry of Defense and most major American and European aerospace or defense contractors. (Redacted) reflects increased participation within autonomous driving systems; so that growth sector may not yet be reflected (more).  Prior highlights follow: (in fairness to subscribers; this is redacted). |

Topping this market, even for the short-term, is a work-in-progress, to say the least. Investors continue sorting 'fact' from mass-media illusion or even delusion, on both sides of the coin.

So far market behavior is within context of the post-Speech spike having a corrective consolidation; preceding this week's forecast test of the highs as we got past the projected Fed rate hike. With so much pending, it's unwise to chase markets higher; but we expected and got shorts run-in yet-again.

Please visit our redesigned www.ingerletter.com website and join us!

So far market behavior is within context of the post-Speech spike having a corrective consolidation; preceding this week's forecast test of the highs as we got past the projected Fed rate hike. With so much pending, it's unwise to chase markets higher; but we expected and got shorts run-in yet-again.

Please visit our redesigned www.ingerletter.com website and join us!

Enjoy the weekend!

Gene

Gene Inger