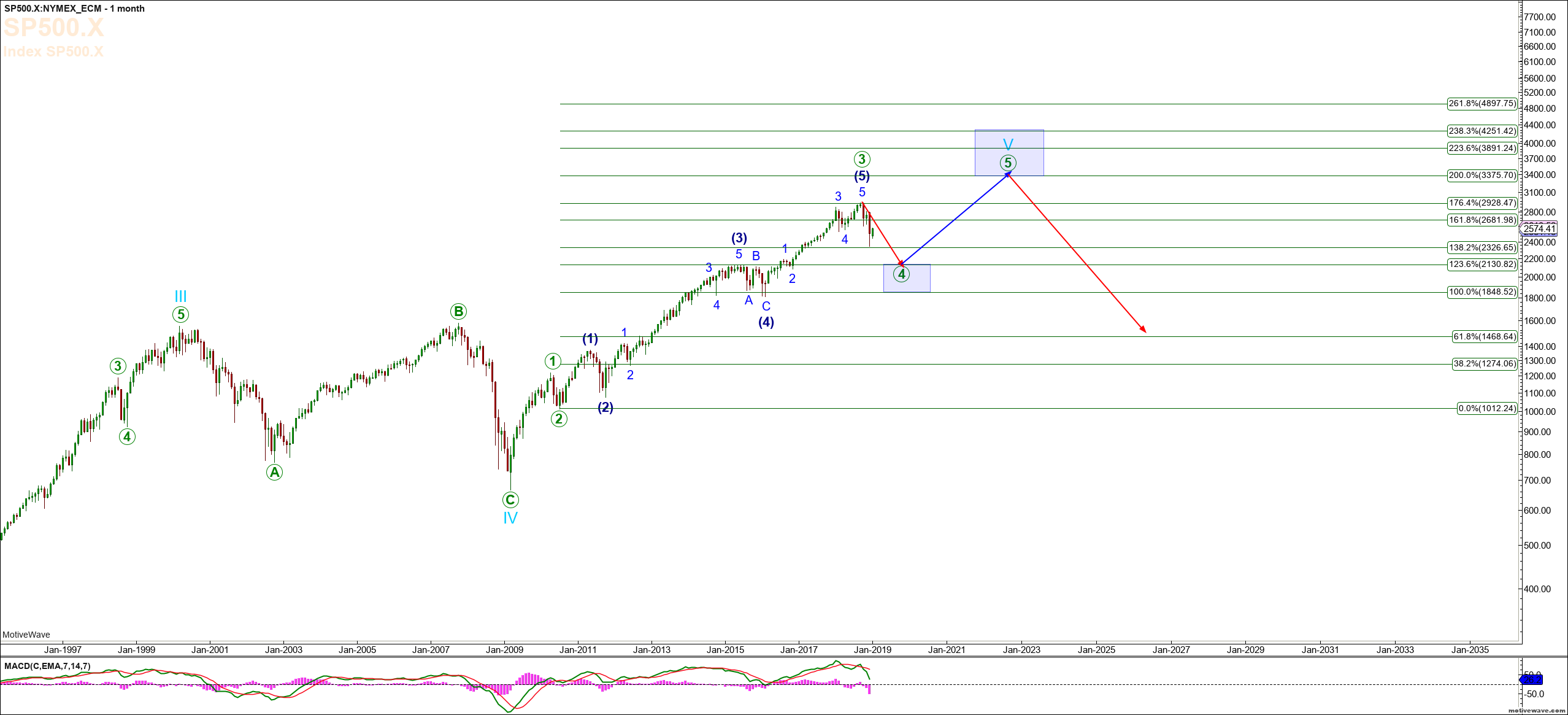

The FED would like SPX to go above 2850 so they can slowly put back at least one more RATE HIKE on the table and quietly do some QT.

Then, SPX goes down to 2600 or lower, the FED assures all it will hold on hikes & QT.....wash, rinse, repeat cycle, until the FED thinks it has reached the optimum rate level and enough QT was accomplished

Doubting The Gods

98% of global assets have posted a positive total return YTD.

But suddenly, price action looks uninspiring again.

A lackluster week even as the central bank "pivot" went global suggests market participants doubt monetary policy has the capacity to fully offset key tail risks.

Equities traded uninspired last week, and that should come as no surprise.

As Deutsche Bank's Aleksandar Kocic put it on Friday evening, "there is a sense of fragile local stability", and that fragility is directly attributable to a lack of visibility around virtually all of the key risks for markets.

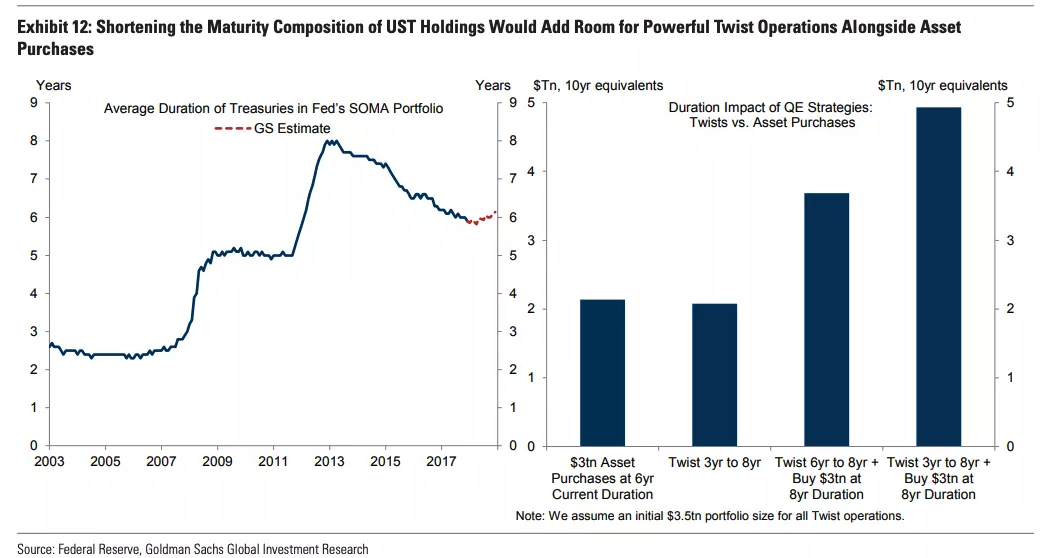

On the left below is the average duration of the Fed’s holdings. On the right, Goldman attempts to show you the asset-purchase equivalent of a new twist based on an initial $3.5 trillion portfolio (the two bars on the left) and also the duration impact of a couple of different combinations of twisting and buying (the two bars on the right).

(Goldman)

Clearly, freeing up room for duration extension down the road (by shortening duration now) is desirable. "As a result, we see an eventual deliberate shift toward shorter Treasury maturities— including bills—as likely," Goldman concluded, in their analysis.

That's been echoed by a number of analysts over the course of the last two months.

The overarching point from all of this is that against a backdrop of seemingly permanent political tumult and proliferating concerns about growth, central banks are again pondering the uncomfortable prospect of being forced to reflate the global economy and rescue risk assets.

The fact that stocks went nowhere this week despite the Fed's dovish pivot and clear signs from policymakers (e.g., the RBA's Lowe) that the global bias is no longer towards tighter policy, suggests the market doubts the ability of central banks to offset the myriad headwinds enumerated here at the outset.

That's not necessarily to say market participants doubt the efficacy of monetary policy itself. Rather, the question is more about whether those policies have been exhausted and if they haven't, whether there's a will to push things even further (e.g., to push rates deep into negative territory and/or resort to outright debt monetization).

The next couple of weeks will be key when it comes to getting a read on whether markets are inclined to view central bank dovishness as "sufficient" when it comes to adding risk (i.e., extending the rally) or whether the accommodative policy pivot is viewed as being already priced in after the best January in more than three decades.

https://seekingalpha...8-doubting-gods