You guys seem to be arguing economics! That's a "dismal" endeavor.

Relax, have "half a glass" and enjoy some good news...While it lasts.

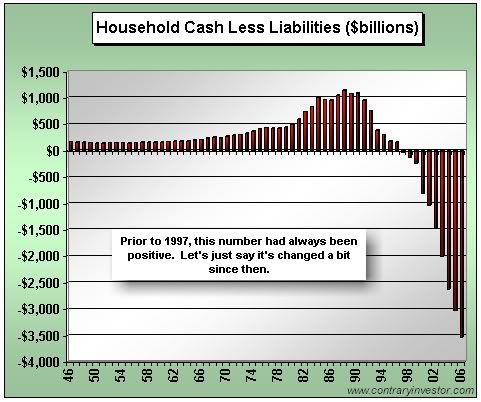

Shhhh! Don't tell anyone.

Started by

Rogerdodger

, Mar 08 2007 09:25 PM

19 replies to this topic

#11

Russ

-

- Traders-Talk User

- 7,199 posts

Member

Posted 08 March 2007 - 11:26 PM

Word of Wisdom Roger. Nothing we can do about it anyways. Actually I misunderstood the post I replied to above. He was talking assets, I thought debts. Ooops.

"Nulla tenaci invia est via" - Latin for "For the tenacious, no road is impossible".

"In order to master the markets, you must first master yourself" ... JP Morgan

"Most people lose money because they cannot admit they are wrong"... Martin Armstrong

http://marketvisions.blogspot.com/

"In order to master the markets, you must first master yourself" ... JP Morgan

"Most people lose money because they cannot admit they are wrong"... Martin Armstrong

http://marketvisions.blogspot.com/

#12

bullshort

-

- Traders-Talk User

- 758 posts

Member

Posted 08 March 2007 - 11:34 PM

Look at the bankruptcy proceedings of Delta, United and a host of other companies that filed for bankruptcy protection. Do a Google search. Among the major liabilities they were or are being relieved of is their pension plan obligations. Arguably, that may be the reason for their BK filings. Those are future liabilities, too, the obligation to pay retirees' pensions. Yet, why is it so important to the future survival of these companies that those obligations be extinguished? It must have some importance since those are among the largest liabilities being erased. And if there's any question that they are being extinguished, ask the retired pilots what the PBGC (Pension Benefit Guarantee Corporation - you know, the equivalent of the FDIC) is covering in terms of the "future" benefits promised by these companies. Private companies like Delta and UA never booked those liabilities in full because the accounting rules didn't require them to. Their pension plans were "actuarily solvent." The American public, the government, is also "actuarily solvent," but the reality is a bit different.

#13

jawndissedi

-

- Traders-Talk User

- 1,018 posts

Member

Posted 08 March 2007 - 11:37 PM

The future's so bright, I gotta

(but that's because I'm short )

)

(but that's because I'm short

)

Da nile is more than a river in Egypt.

#14

pdx5

-

- Traders-Talk User

- 9,529 posts

I want return OF my money more than return ON my money

Posted 08 March 2007 - 11:41 PM

One of the outfits I worked for and was receiving pension from upon reaching 55

went bankrupt. (Mainly because I had left the outfit, hahaha). But PBGC took over

and I am still getting 100% of my previous pension from PBGC.

"Money cannot consistently be made trading every day or every week during the year." ~ Jesse Livermore Trading Rule

#15

bullshort

-

- Traders-Talk User

- 758 posts

Member

Posted 08 March 2007 - 11:51 PM

One of the outfits I worked for and was receiving pension from upon reaching 55

went bankrupt. (Mainly because I had left the outfit, hahaha). But PBGC took over

and I am still getting 100% of my previous pension from PBGC.

I take everything back, the system is undoubtedly working just fine. Now, if I could just find the key to that Social Security lockbox.

#16

TradeMark

-

- Traders-Talk User

- 809 posts

Member

Posted 08 March 2007 - 11:57 PM

Pdx5

Could not find article I had but found one even better and more up to date. That is good news.

Bad news is that the numbers are even worse. This is from a Federal Reserve publication just last summer. Scholarly treatment, but worth the read if you really want to understand this issue..

http://research.stlo...7/Kotlikoff.pdf

Best

TM

Could not find article I had but found one even better and more up to date. That is good news.

Bad news is that the numbers are even worse. This is from a Federal Reserve publication just last summer. Scholarly treatment, but worth the read if you really want to understand this issue..

http://research.stlo...7/Kotlikoff.pdf

Best

TM

#17

OEXCHAOS

-

- Admin

- 22,026 posts

Mark S. Young

Posted 09 March 2007 - 07:11 AM

Setting aside your trading gains, of course ( rolleyes.gif ), does anyone feel like their net worth is truly increasing at the pace cited in this article (California residents not eligible to respond [just kidding])?

I'm not typical, by any means, but I'm thinking my net worth increased that much or more last year. Decrease the debt, make a little more, save a little more, have a decent year in the IRA...it all adds up.

But note, my assets aren't yet my government's to confiscate. They only get to mess with income. Further, the "unfunded liabilities" will for some and at the margins remain unfunded--forever and for a variety of reasons.

M

I'm not typical, by any means, but I'm thinking my net worth increased that much or more last year. Decrease the debt, make a little more, save a little more, have a decent year in the IRA...it all adds up.

But note, my assets aren't yet my government's to confiscate. They only get to mess with income. Further, the "unfunded liabilities" will for some and at the margins remain unfunded--forever and for a variety of reasons.

M

Mark S Young

Wall Street Sentiment

Get a free trial here:

http://wallstreetsen...t.com/trial.htm

You can now follow me on twitter

#18

Cirrus

-

- TT Patron+

- 5,735 posts

Member

Posted 09 March 2007 - 07:30 AM

Net worth of U.S. households skyrockets

By JEANNINE AVERSA, AP Economics Writer Thu Mar 8, 5:27 PM ET

WASHINGTON - The net worth of U.S. households climbed to a record high in the final quarter of last year, boosted mostly by gains on stocks, the

Federal Reserve reported Thursday.

Net worth the difference between households' total assets, such as houses and bank accounts, and their total liabilities, such as mortgages and credit card debt, totaled $55.6 trillion in the October-to-December quarter.

That marked a 2.5 percent growth rate from the third quarter, the previous quarterly record high. Stocks gains helped fuel the increase in net worth, although real-estate gains played a role, too.

For all of last year, households' net worth rose by 7.4 percent, a slower pace than the 7.9 percent increase registered in 2005.

Household debt, meanwhile, grew by 8.6 percent in 2006, down from a 11.7 percent increase in the prior year. The Fed said this deceleration "was accounted for by much slower growth of home mortgage debt."

Home mortgage debt growth slowed to a 8.9 percent last year, compared with a 13.8 percent increase in 2005. This year's growth in home mortgage debt was the smallest increase in six years.

After a five-year boom, the housing market fell into a deep slump last year. Sales cooled. So did home prices, which had been galloping ahead, making consumers feel more wealthy and more inclined to spend.

Economists said Thursday's report suggest households' finances are holding up fairly well to any strains caused by the troubled housing market and well as some sluggishness in overall economic growth. Analysts said that's because the jobs climate remains in good shape and income growth has picked up.

"Slower growth in some of the nation's high-flying housing markets was not enough to send net worth south in the fourth quarter," said Gina Martin, economist at Wachovia. "Instead, household balance sheets continued to improve, as growth in liabilities continued to slow, while growth in assets held steady."

One risk facing the economy is that the housing slump will take an unexpected turn for the worse, a development that likely would cause consumers to clamp down. That could spell trouble for overall economic activity.

The question you must ask is what % of Americans have a large enough stock portfolio to have produced that type of gain. I'm no liberal by any means, but it's a factor of the wealthiest 5-10% of American's portfolio 'carrying the load' for everyone.

#19

Rogerdodger

-

- TT Member*

-

- 26,877 posts

Member

Posted 09 March 2007 - 09:46 AM

have a decent year in the IRA

+40%

"Nature's Failure to Function in a 'Predictable Way'... 500 years ago?"

BIGGEST SCIENCE SCANDAL EVER...Official records systematically 'adjusted'.

BIGGEST SCIENCE SCANDAL EVER...Official records systematically 'adjusted'.

#20

calmcookie

-

- Traders-Talk User

- 2,536 posts

calmcookie

Posted 09 March 2007 - 10:09 AM

Waaaaaa  Now everyone knows!

Now everyone knows!

Now everyone knows!