It turned out to be another volatile week of trading with Chairman Powell's comments on Wednesday providing renewed fuel for the bulls to work with as the markets finished things on Friday with a average gain of +1.02%, with the NASDAQ Composite leading the pace with a gain of +2.09%. For the month of November, the major market indices closed at or near their highs for the month with an average gain of +5.39%. This brought the 4th quarter average gain since the October 13th lows to a whopping +15.58%, and now cutting the average losses for the year to -12.43%.

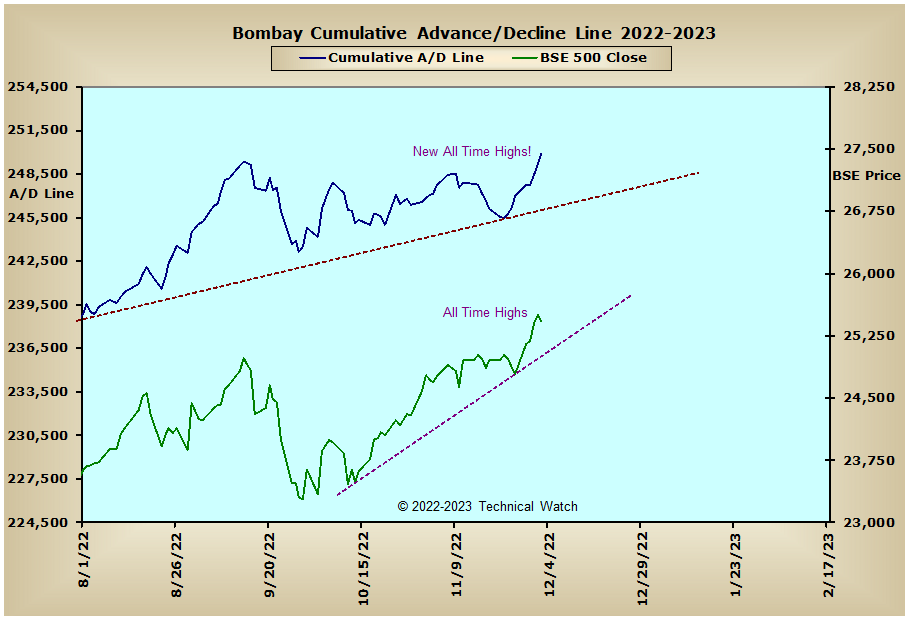

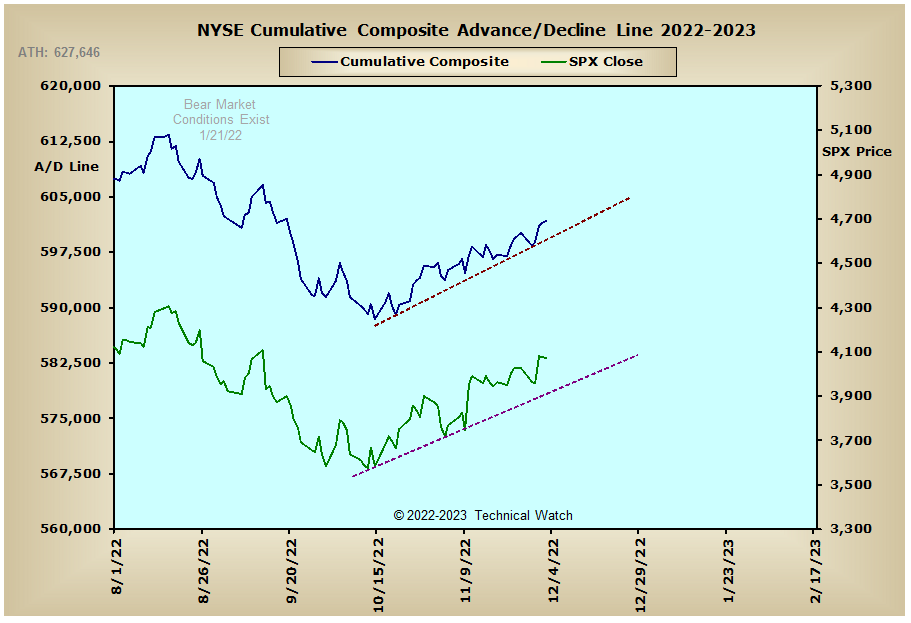

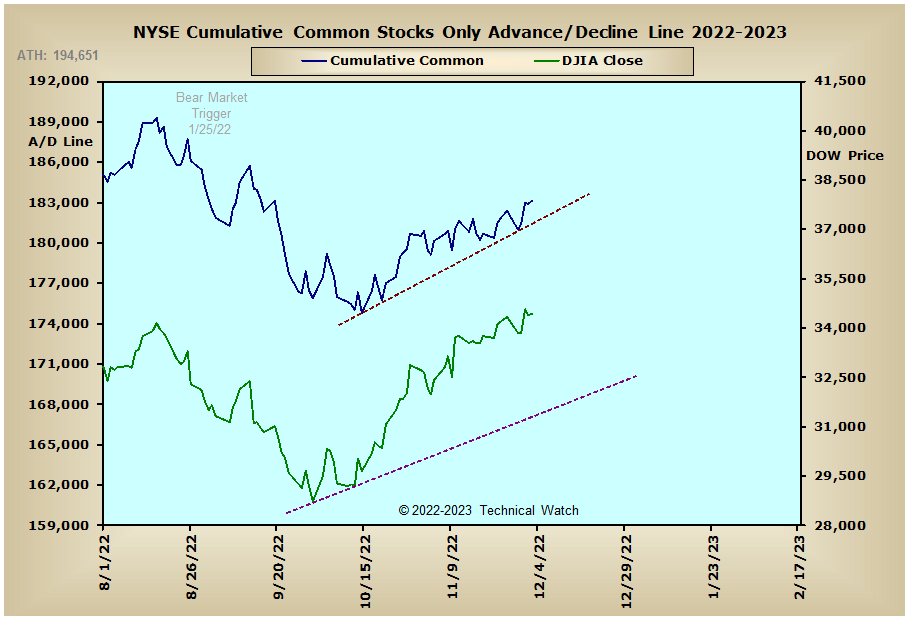

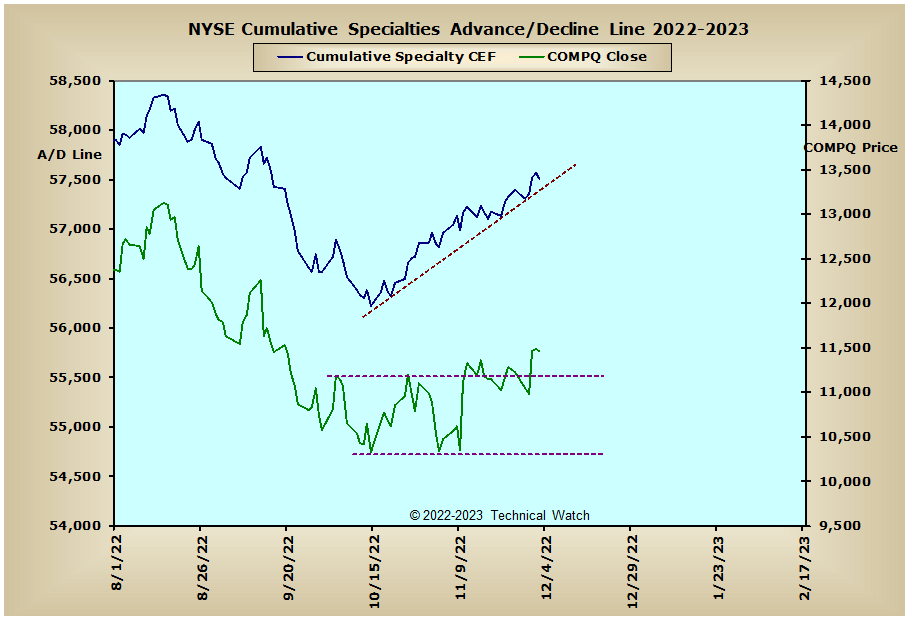

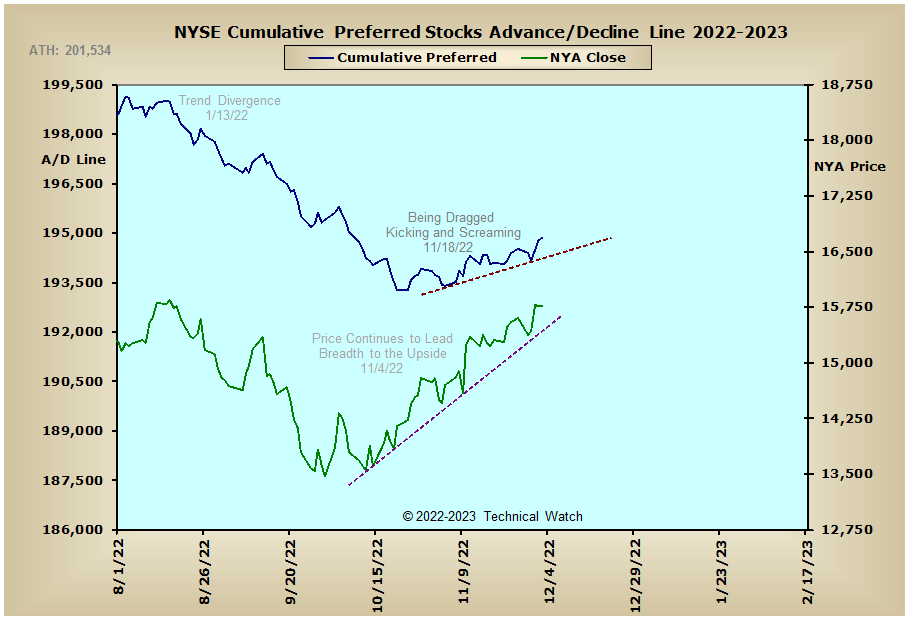

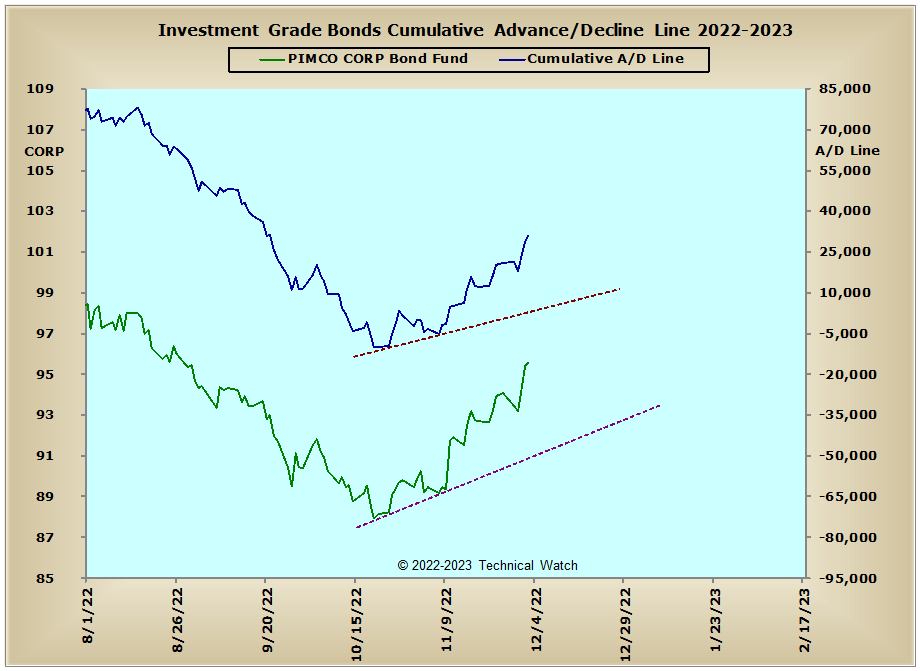

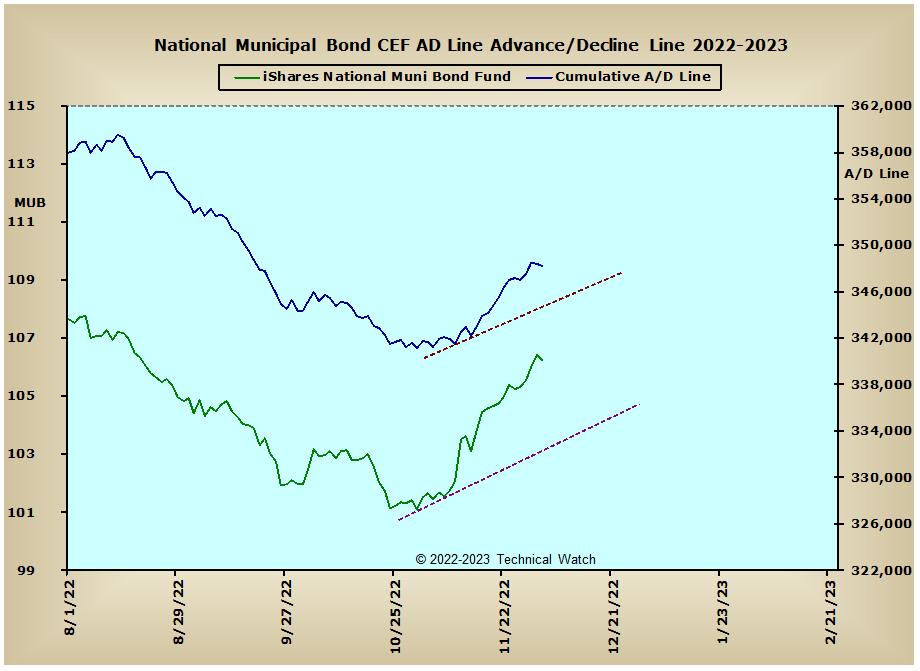

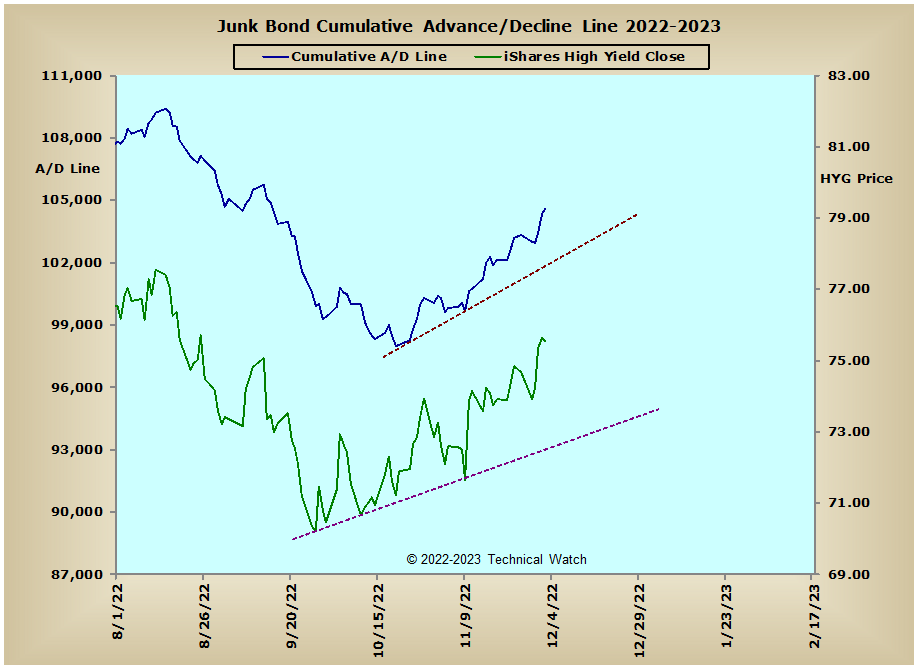

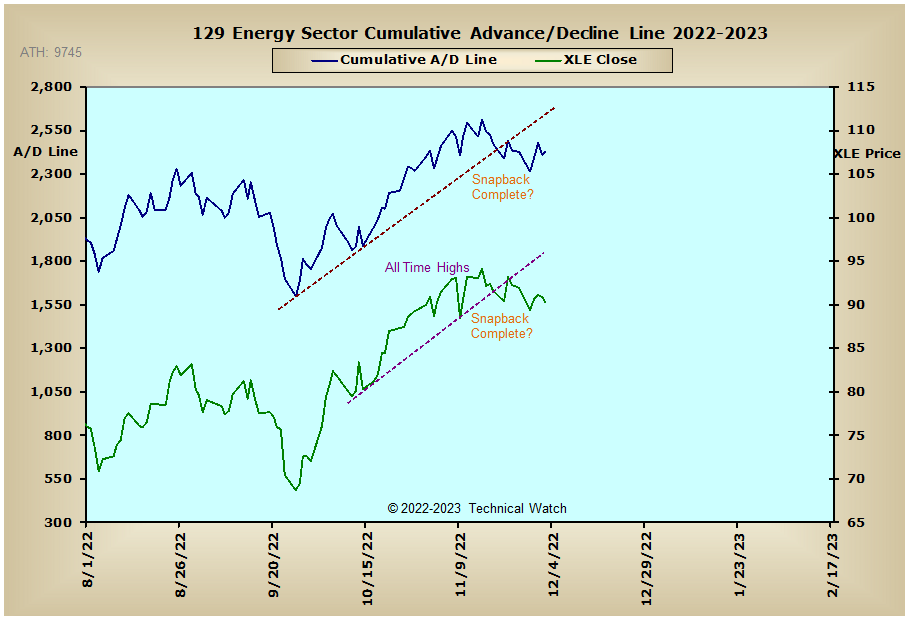

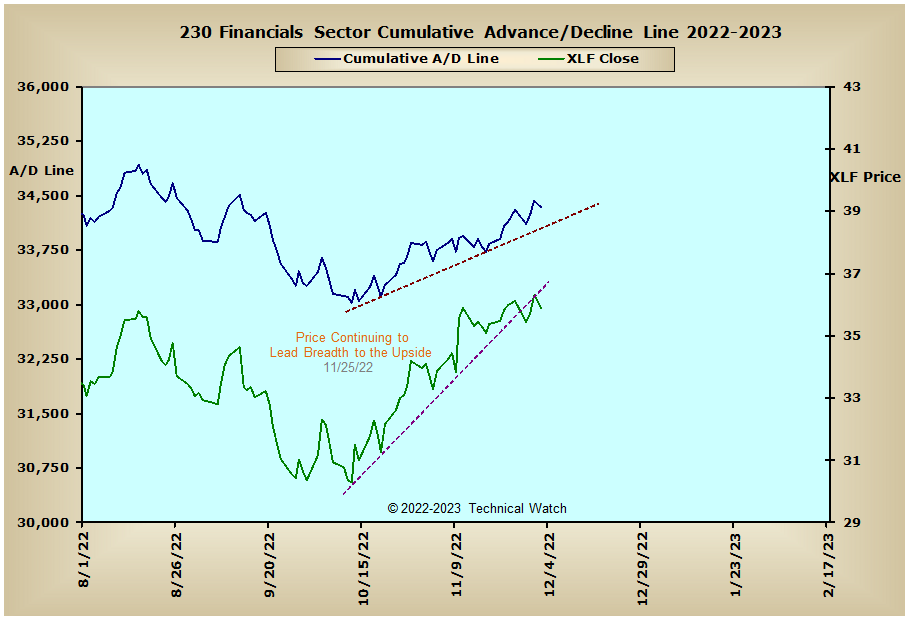

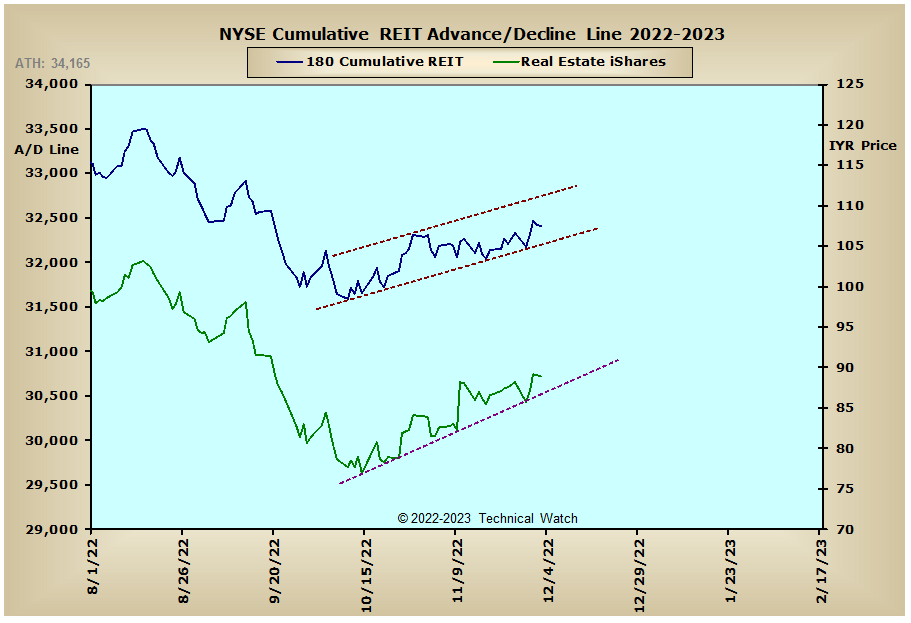

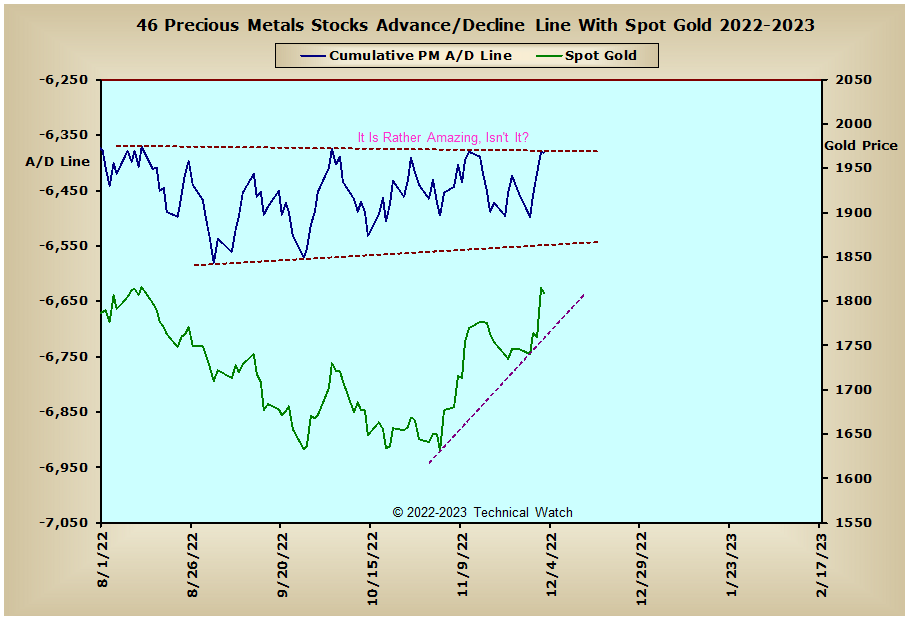

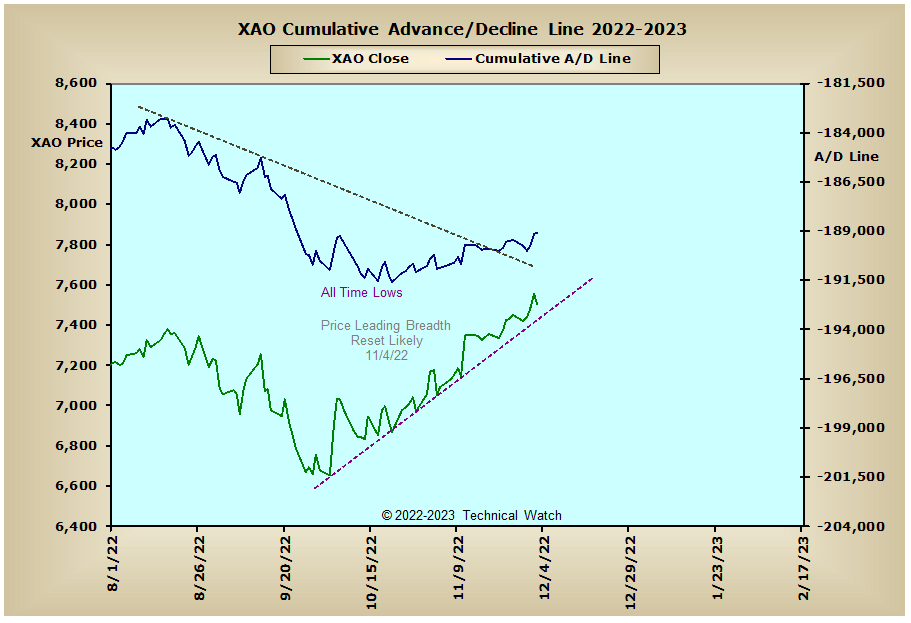

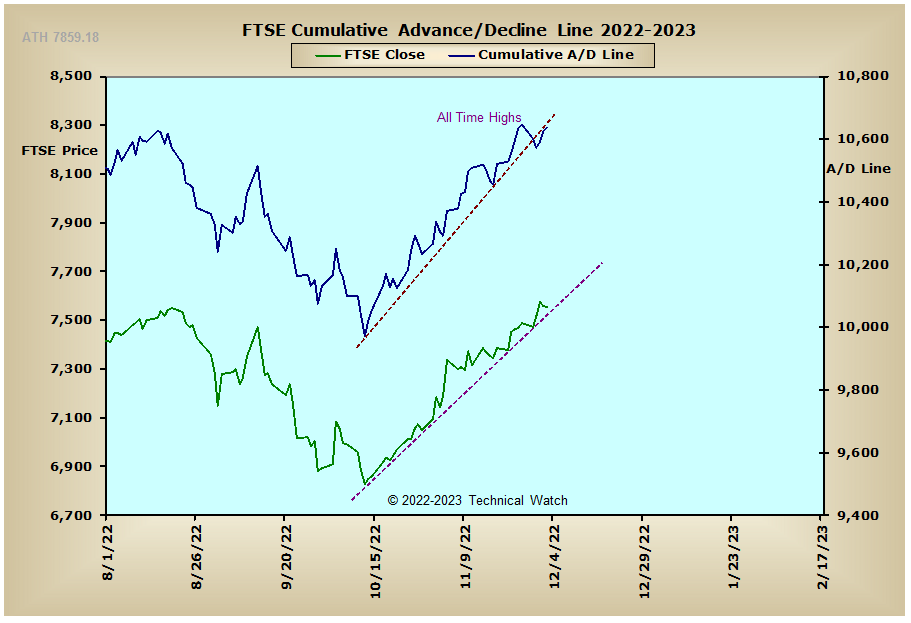

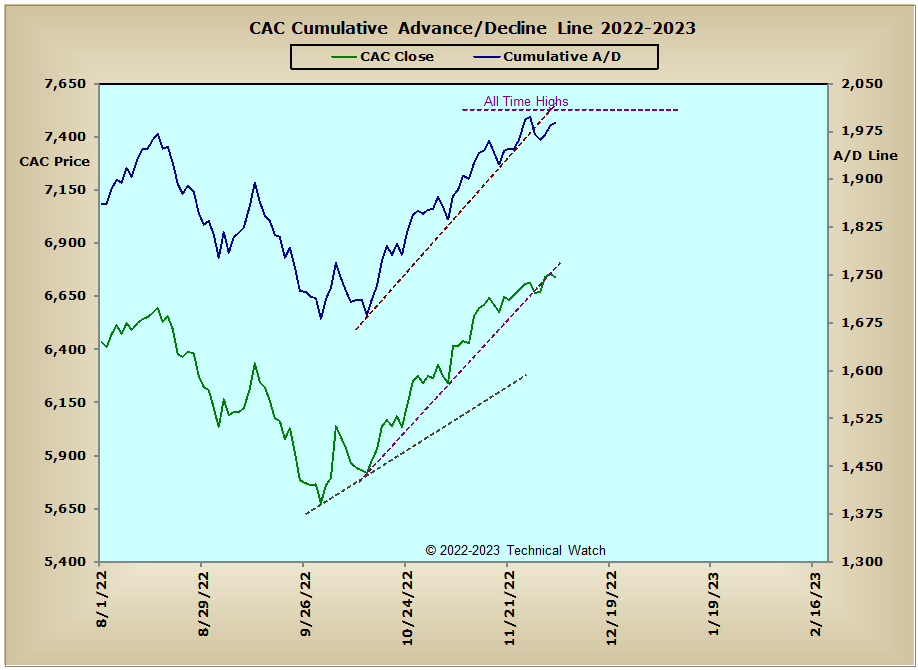

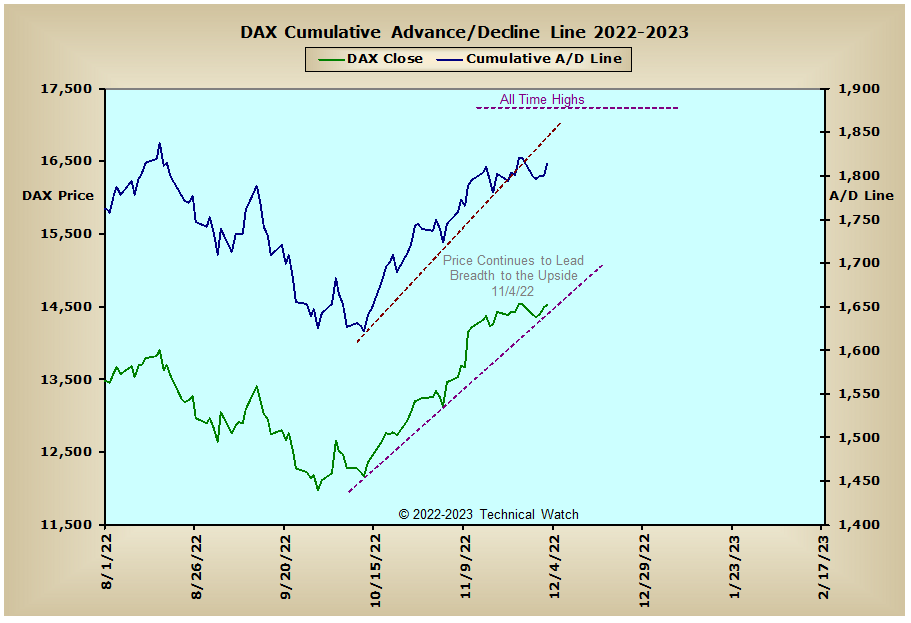

Looking over this week's updated array of cumulative breadth charts shows that both equity related and interest rate sensitive issues have maintained their trends to the upside with the exception of the Russell "1987" advance/decline line which continues to narrowly hold onto bearish divergence at this time. European markets also continue to show good underlying support as the CAC, DAX and FTSE advance/decline lines flirt with their all time highs, while over in India, both the Bombay advance/decline line and the Bombay 500 itself moved to new all time highs this past week as India continues to enjoy making up for any manufacturing losses by China's ongoing "COVID Zero" policies. Although the price of both gold (+3.17%) and silver (+8.49%) had solid gains for the week on the back of Chairman Powell's bullish comments on interest rates, both the Precious Metals and XAU advance/decline lines continue to be contained within their 3 month channels. With the FedWatch tool continuing to suggest that the December 14th meeting will see another 1/2% hike in rates, and another 1/4% on February 1st before a pause is considered, it would now appear that the December jobs and inflation numbers to be released in January will be far more important to any critical changes to interest rate policy for the 1st and 2nd quarters of 2023.

So with the BETS moving up to a reading of -20, traders and investors are back to a more neutral view of market activity despite the severe non confirmation when comparing the BETS to the price of the New York Composite Index. One exciting thing for the longer term bulls that we briefly touched upon in the chat room this past week is that the traditional NYSE breadth McClellan Summation Index has just fulfilled one ingredient of a "Summation Index Bull Market Signal" by finishing with a reading on Friday of +2070 after bottoming out on October 13th at -2645...and did so in 7 weeks time. The general rule is that we usually see a MCSUM structure of a 3 wave "stair step" pattern of advance from below the -1500 level to above +2000 within a 20 to 23 week period for this signal to be triggered. Being that this analytical observation by Sherman and Marian McClellan was shared back in 1970, one has to wonder if the rules have changed over time due to: more companies and shares being traded, technological advances, and a more global scope of trading executions. But in any event, the amount of investment capital coming back into the NYSE over the last 2 months has been massive enough to at least stabilize equity prices as we go into next year if not put an end to current bear market conditions....especially with the global markets as robust as they are currently. Meanwhile, the NYSE Open 10 TRIN remains in "oversold" territory with a reading on Friday of 1.07, while the 10 day average of the equity put/call ratio rose significantly into midweek to the highest levels of put buying since the COVID crash of 2020 before being blown out the water by Chairman Powell's comments and implied put premiums collapsing. With 3rd quarter productivity and November PPI numbers the main focus for the week ahead, the markets should continue to have enough internal buoyancy to remain "on trend" as we go into this month's quarterly OPEX on the 16th. With all this as a backdrop then, investors should remain on the sidelines while watching sector rotation, while traders are now back to "hit and run" strategies that will likely remain in effect until the end of the year.

Have a great trading week!

US Equity Markets:

US Interest Rates:

US Sectors:

Precious Metals:

Australia:

England:

France:

Germany:

India: